When One MSA Serves Three Revenue Types, You Lose the Renewal

Contract governance is where pricing strategy either holds or quietly unravels. Hybrid-revenue companies: B2B2B platforms, freight, marketplaces, hardware+services, distribution: are where that unraveling happens fastest. This guide is the operator's playbook for rebuilding contract discipline when one template cannot serve three revenue types.

The Operator's Guide to Contract Governance Across Revenue Architectures

There is a quiet moment, usually two years after a commercial pivot, when the head of legal ops realizes the contract portfolio no longer matches the business. The logos, signatures, and numbers are mostly right. But the terms inside: renewal mechanics, indexation, liability carve-outs, grandfather clauses written for a business model that no longer exists: tell a story of a company that used to be something simpler. This guide is for operators who recognize that moment and want to act on it before the next renewal exposes it.

TL;DR

Single-template contracting fails the moment a company earns revenue in more than one way. Hybrid-revenue operators: forwarders who also broker, platforms who also license, manufacturers who also service: need a governance system built on three disciplines: master templates with approved variants, a quarterly audit run by a cross-functional council, and price-indexation treated as a first-class pricing decision rather than a legal afterthought. The operators who get this right do not have prettier contracts. They have fewer disputed renewals, shorter cycles, and a pricing strategy that survives contact with the pipeline.

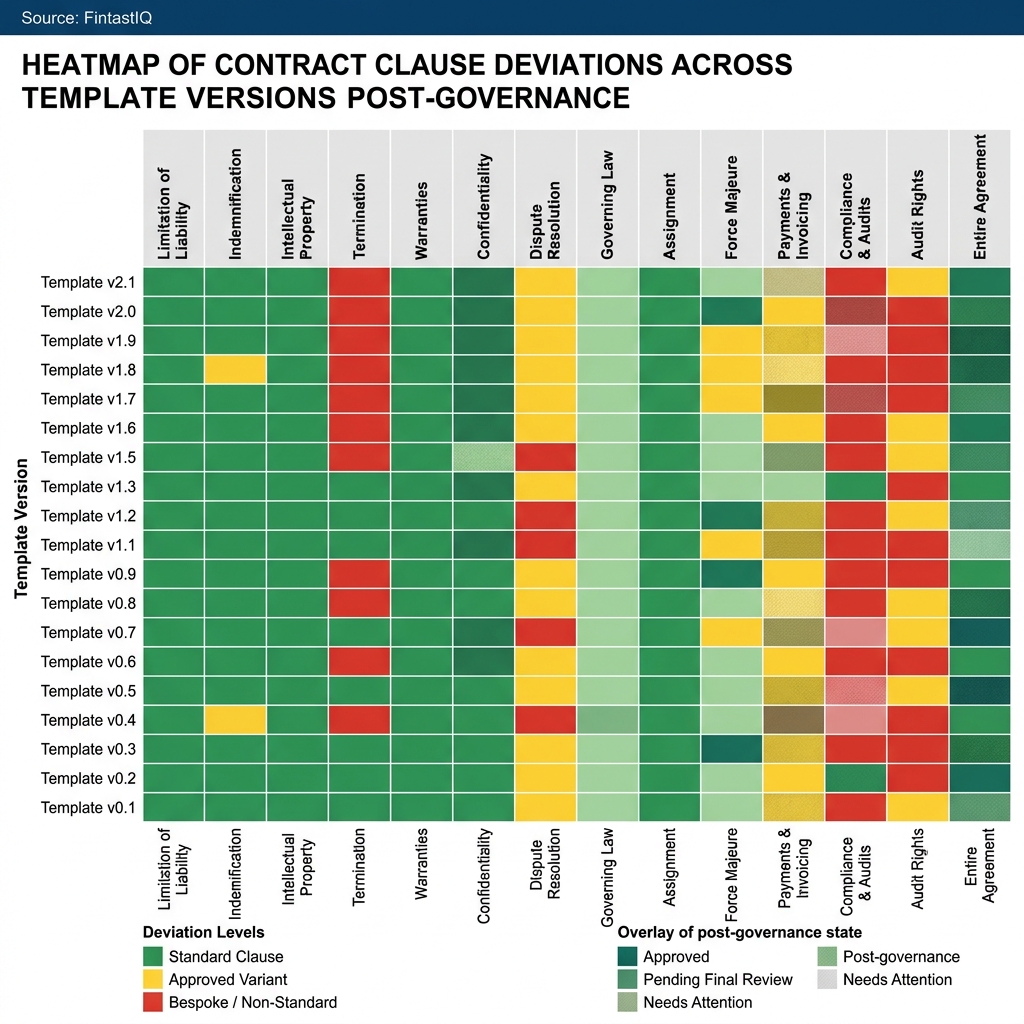

Exhibit: Contract-variant heatmap by revenue type

Exhibit: Contract-variant heatmap by revenue type

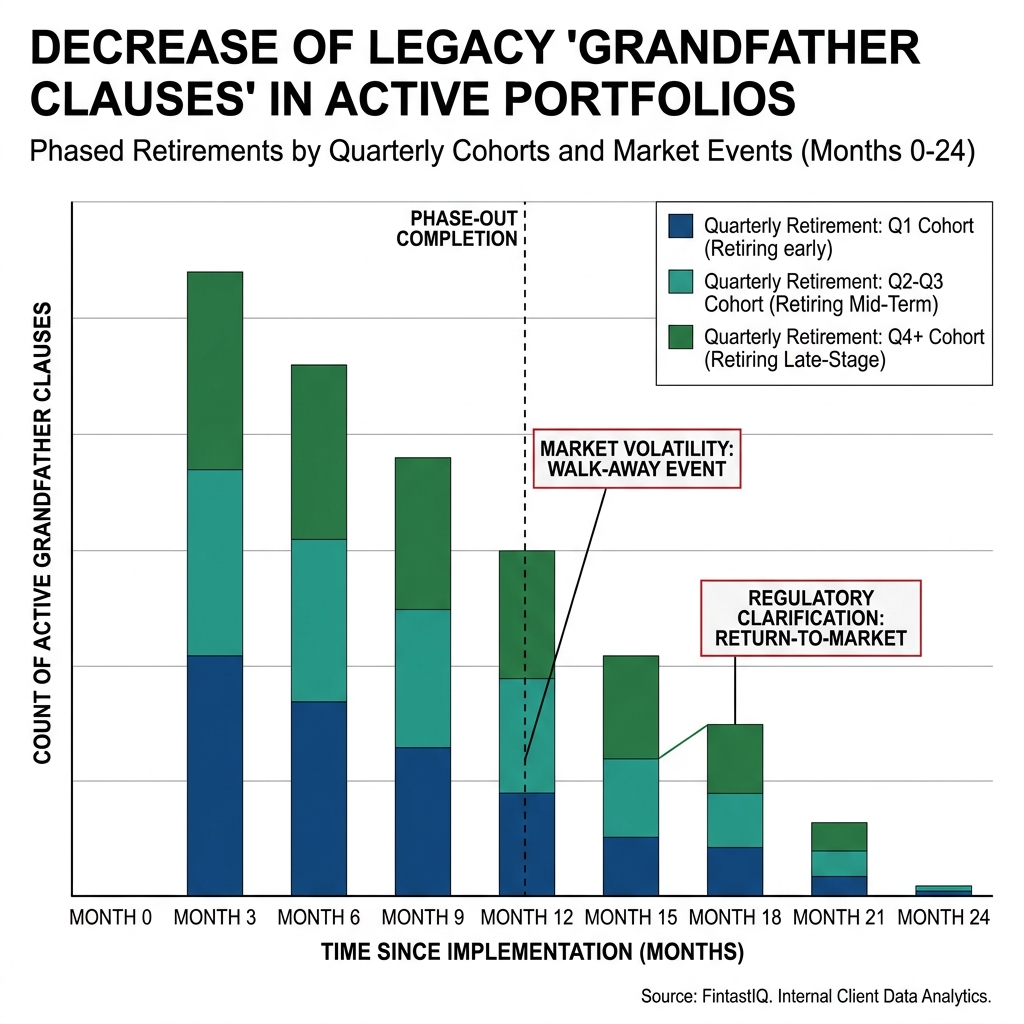

Exhibit: Grandfather-clause cohort retirement timeline

Exhibit: Grandfather-clause cohort retirement timeline

The core problem: a contract portfolio that outgrew its templates

Halyard & Crest Freight is a 175-person, $120M-revenue business that earns money in three distinct ways. Forty-eight percent of revenue comes from the forwarder business, where Halyard & Crest takes title risk and margin on a managed lane. Thirty-four percent comes from the brokerage business, where the company matches 1,200 shippers against 3,400 carriers across 24 trade lanes and earns a spread. Eighteen percent comes from the platform SaaS business, where shippers and carriers subscribe to visibility and tender-management tools regardless of whether Halyard & Crest moves the freight. Three revenue types. One legal team. One master services agreement that was originally drafted when the company was only a forwarder.

When Tomás took over as head of legal ops, he inherited the predictable consequences. Four thousand eight hundred active contracts across the three revenue types. Twenty-two template versions in circulation, because every time sales encountered a clause that did not fit, a lawyer either drafted a variant or, more often, pasted language from the last deal that closed. Eighteen percent of the portfolio carried grandfather clauses more than two years stale: pricing structures, service levels, or liability caps that had survived multiple renewals because no one had the mandate to retire them. Eleven percent of active contracts had no price-indexation terms at all, which in a freight business where diesel and driver wages move quarterly is not a drafting gap, it is a margin leak. In a single quarter Halyard & Crest had four contested renewals: four shippers simultaneously arguing that their contract permitted something the business no longer wanted to permit.

The best operators compete on discipline, not instinct. Tomás understood the portfolio was not broken because the lawyers were bad or the salespeople aggressive. It was broken because the governance system had never been rebuilt to match the revenue architecture. Three revenue types need three master templates, not twenty-two versions of one. A portfolio of 4,800 contracts needs an audit rhythm, not an annual scramble. A hybrid business needs indexation written into every template, not negotiated deal-by-deal. The rebuild that followed is the subject of this guide.

Part One: Why single-template contracts fail hybrid-revenue companies

Single-template contracting is the default up to about $50M in revenue, for good reason. One template is faster, easier to train sales on, and lets legal mostly say yes to redlines because the underlying structure is stable. The problem is that single templates encode a theory of how the business makes money, and when the business starts making money in more than one way, the template begins to lie about the business.

At Halyard & Crest, the original forwarder MSA assumed the company took title risk, liability followed the cargo, price was a negotiated rate per lane, and renewal was annual. Every one of those assumptions was wrong for the brokerage business, where Halyard & Crest never takes title, liability attaches to the carrier, pricing is a spread, and renewals are rolling. They were also wrong for the platform SaaS business, where the product is software, liability is capped at fees paid, pricing is a subscription, and renewals are auto-renewing. Sales teams papered over the mismatches with side letters, amendments, and clause substitutions. That is how you end up with twenty-two template versions. The template did not proliferate because anyone wanted it to. It proliferated because one template was being asked to do three jobs.

The symptoms are consistent across industries. Renewal cycles stretch because every redline needs a legal-commercial-finance huddle to decide which version of which clause applies. Pricing strategy leaks into the contract: a year-one discount becomes a year-three grandfathered floor. Indexation terms that protect margin in one revenue type become a ceiling in another. Most dangerous, sales learns the contract is negotiable in ways pricing never authorized, because the template's gaps are where creative redlines live. Pricing is a signal before it is a number, and a portfolio full of bespoke variants signals that the company does not know what its own price is.

Part Two: Master templates, approved variants, and sunset discipline

The rebuild at Halyard & Crest started with a subtraction. Twenty-two template versions collapsed into three master templates: one for the forwarder business, one for the brokerage business, one for the platform SaaS business. Each master template encodes the commercial theory of that revenue type: who takes what risk, how price is set, how price moves, how the relationship renews, how it ends. The master templates are short. They are not the place for creativity. They are the place for consistency.

Creativity lives in the approved variants. The council authorized fourteen approved variants: four or five per master template: to handle situations that recur. A large-shipper variant of the forwarder template that raises the liability cap in exchange for a longer commitment. A carrier-marketplace variant of the brokerage template that adjusts the payment cycle. A multi-year SaaS variant that trades a rate lock for a usage floor. Each is pre-negotiated, pre-approved by legal, finance, and commercial, and documented with the exact conditions under which sales may offer it. A variant is not a discount. It is a pre-blessed deviation. Anything outside the approved variants is a non-standard clause, and non-standard clauses are where governance lives or dies.

The third piece is sunset discipline. Every non-standard clause that enters the portfolio: whether through a side letter, an amendment, or a negotiated redline: carries a ninety-day sunset. At the end of ninety days, the clause either becomes an approved variant (because it has appeared in enough deals to be worth systematizing), or it is retired in the next renewal. Sunset discipline is the mechanism that prevents the portfolio from drifting back to twenty-two versions. Pricing maturity is measured by what you stop doing, and the ninety-day sunset is how Halyard & Crest stops doing bespoke contracting at scale. Two quarters after implementation, template versions dropped from twenty-two to fourteen: three masters plus eleven variants still in active use, with three variants retired because no deal had re-triggered them in ninety days.

Part Three: The quarterly audit rhythm and the cross-functional council

Templates and variants are the static architecture. The audit rhythm is the dynamic one. Halyard & Crest runs a quarterly contract audit against the full 4,800-contract portfolio, and the audit is owned by a seven-person cross-functional contract council: two from legal, two from commercial, one from finance, one from pricing, and Tomás as chair. The council does not draft contracts. The council governs the system that drafts contracts.

Each audit answers four questions. First, which contracts are drifting from the master template or variant? Drift is measured by clause-level diff against the canonical version: anything above a defined threshold is flagged for renewal review. Second, which grandfather clauses are stale? A grandfather clause that has survived two or more renewals without re-examination is presumptively retired at the next renewal unless the council keeps it. In two quarters this one rule retired stale grandfather clauses across 340 contracts. Third, which indexation terms are firing correctly? The pricing member runs the indexation math against actual rate movement, and any divergence goes on the escalation list. Fourth, which non-standard clauses have crossed the ninety-day sunset and need to be promoted or retired?

The council's role is governance, not firefighting. Discounting is usually a symptom: a template that does not fit the deal, a variant that was never approved, a pricing policy sales cannot execute. When the same non-standard clause appears in three deals in a quarter, that is not a contract problem, it is a product or pricing problem, and the council routes it upstream rather than patching downstream. The quarterly cadence is fast enough to catch drift and slow enough to see patterns. A council that meets only in crisis is a committee. A council that meets every quarter is governance.

Part Four: Price-indexation and escalation as first-class pricing decisions

Most contracts treat indexation as boilerplate: a CPI clause pasted near the end of the commercial terms, rarely read, rarely enforced. In a hybrid-revenue business, and especially in one exposed to input-cost volatility like freight, indexation is not boilerplate. Indexation is a pricing decision, and it deserves the same rigor as the headline rate.

The Halyard & Crest rebuild standardized indexation across all three master templates with two components. The first is a published index floor: CPI for the SaaS product, a blended CPI-plus-freight-rate index for the forwarder and brokerage businesses, with the freight-rate component tied to a public benchmark rather than the company's own cost data. Tying the index to a public benchmark removes the negotiation from whether the index fired and puts it on whether the benchmark is the right one. The second is an asymmetric floor: the index moves price up when inputs rise, and price moves down only when the counterparty affirmatively renegotiates. That asymmetry is how the business captures the margin of falling input costs rather than giving it back by default. It is not aggressive. It is the pricing theory of the business written into the contract, which is what an indexation clause is for.

Tomás's walk-away moment is worth naming. Midway through the rebuild, a $2.4M shipper on annual renewal asked for a unilateral carve-out from the new indexation standard: a return to the old, un-indexed pricing that had been costing Halyard & Crest margin for three years. The shipper framed it as a relationship request. The council framed it as a pricing decision. Tomás walked away. Sixty days later the shipper returned and signed the standard terms. The walk-away worked because Tomás had a defensible standard to walk back to. Without the rebuild, it would have been a gamble. With the rebuild, it was policy. Two quarters in, disputed renewals dropped from four to one. Average contract cycle time compressed from forty-two days to eighteen. Those are pricing numbers expressed through the contract portfolio.

Three failure modes to name before you see them

Template proliferation. What got Halyard & Crest to twenty-two versions. It starts when a single deal gets a custom clause because the pipeline matters more than the template. It compounds when the custom clause gets pasted into the next deal, then the next, until the template of record is whichever version was last used. Template proliferation is never caused by lawyers. It is caused by the absence of a governance forum that answers "should this be a variant" in writing within a defined window.

Grandfather rot. Old terms survive renewals because no one has the explicit mandate to retire them. A 2021 price floor becomes a 2023 renewal and then a 2025 renewal, not because anyone decided it should, but because the renewal process defaults to carrying language forward. Grandfather rot is measurable: at Halyard & Crest, eighteen percent of the portfolio: and fixable only with a presumption of retirement at the audit layer.

Sales-led contract drift. The contract becomes the place where sales negotiates what pricing did not. A denied discount shows up as a payment-term concession. A volume commitment that could not be agreed shows up as an exclusivity carve-out. Sales-led drift is the most dangerous of the three because it routes around the pricing function while appearing to respect it. The only defense is a council with authority to read every non-standard clause against the pricing policy it should have been.

The 30-60-90 sprint

Days 0-30. Map the portfolio. Count active contracts by revenue type. Count template versions. Measure drift at the clause level. Flag grandfather clauses older than two renewal cycles. Identify contracts with missing or misfiring indexation. Do not fix anything yet. The first thirty days exist to make the mess legible. At Halyard & Crest, this phase produced the 22-versions, 18-percent-stale, 11-percent-missing-indexation numbers that made the rebuild possible.

Days 31-60. Draft the three master templates and the first cut of approved variants. Stand up the council with a written charter: who is on it, what it decides, what it escalates, how often it meets. Publish the ninety-day sunset rule. Do not touch live renewals yet. Build the architecture so that when it meets the portfolio, it meets with authority.

Days 61-90. Run the first quarterly audit against the full portfolio using the new masters and variants as the canonical reference. Produce the drift list, the grandfather-retirement list, the indexation-correction list, and the sunset list. Commit to the first wave of corrections at the next renewal window. Report back to commercial leadership with one metric: what percentage of the portfolio aligns to a master or approved variant. At Halyard & Crest, that number moved from thirty percent to seventy-eight percent in two quarters.

FAQ

How do we know if we have a hybrid-revenue problem and not a messy template library? Count your template versions. More than one master template for the same revenue type is a hygiene problem. A single master template serving two or more economically distinct revenue types: different risk, different pricing mechanics, different renewal logic: is a hybrid-revenue problem, and hygiene alone will not fix it. The test is whether the commercial theory of the contract matches the commercial theory of the revenue. If the contract assumes you take title and you no longer do, the template is lying about the business.

Who should chair the contract council: legal, commercial, or finance? Legal operations is the right default chair because the role requires neutrality across the three functions and because the work product is a governed portfolio. A commercial chair tends to under-weight drift risk because pipeline pressure is immediate and drift is abstract. A finance chair tends to under-weight deal velocity because margin protection is concrete and cycle time is not. A legal-ops chair with explicit authority to escalate to the CRO and CFO, and a written charter that says what the council decides without escalation, produces the fastest durable governance. Authority on paper matters more than reporting line.

Is a ninety-day sunset on non-standard clauses realistic in a long-cycle business? The ninety days is the review trigger, not the retirement deadline. At ninety days the council decides one of three things: promote to an approved variant, retire at next renewal, or extend the sunset for one more cycle with a written reason. In long-cycle businesses the extend decision happens more often, which is fine. What the rule prevents is the quiet persistence of a non-standard clause that no one has revisited. Ninety days forces the revisit. The decision is still judgment, but the revisit is automatic, and that is the whole point.

How should indexation be structured when inputs are volatile and public benchmarks are imperfect? Use a blended index tied to a public benchmark plus a smaller negotiated component. The public component removes the argument about whether the index fired. The negotiated component absorbs the gap between the public benchmark and your actual cost exposure. Publish the formula in the master template so that the indexation math is not a negotiation at renewal. Asymmetry: price moves up on index, moves down only on affirmative renegotiation: is a pricing choice, not a default, and should be made deliberately at the template level rather than quietly in a side letter.

What is the right cadence for a contract audit in a 4,800-contract portfolio? Quarterly for the governance layer (drift, grandfather, indexation, sunset). Monthly for the operational layer (renewal windows, active redlines, escalations). Annually for the strategic layer (master-template refresh, variant rationalization, charter review). The mistake most operators make is conflating the three cadences into a single annual review, which is why annual reviews feel like archaeology. Separate the cadences and each one becomes manageable. Tomás's council runs the quarterly layer; the commercial-ops team runs the monthly layer; the executive team runs the annual layer.

How do we prevent the contract council from becoming a committee? Three mechanics. First, a written charter that defines what the council decides without escalation and what it must escalate. Second, a fixed quarterly calendar that does not move for pipeline pressure. Third, a published decision log: every non-standard clause, every grandfather retirement, every variant promotion, recorded with the reason. Committees drift because their decisions are invisible. Councils hold because their decisions are on the record. The decision log is the artifact that converts a recurring meeting into governance and produces the evidence base that makes the next quarter's decisions faster.

When is it right to walk away from a renewal over contract terms? When the ask violates a standard you have documented, priced, and applied consistently to comparable customers. The walk-away works because it is policy, not mood. Tomás walked away from a $2.4M renewal over a unilateral indexation carve-out because the indexation standard was in every master template and had been held on every other renewal that quarter. The shipper returned at sixty days because the standard was credible across the portfolio. Walking away from a deal without a documented standard is a gamble. Walking away with one is a negotiation that ends in a better place for both sides.

How does this apply to PE portfolio companies with multiple operating models? PE portfolios are hybrid-revenue at the fund level, even when each portfolio company is pure-play. The model transfers with one adjustment: the council operates at the portfolio-company level, but a shared template library and shared indexation methodology across the fund produces compounding value at exit. Portfolio companies with governed contract estates diligence cleaner, renew faster, and show higher revenue quality in the data room. Contract governance is not a cost center in PE. It is a valuation input, and operators who treat it that way exit better.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

3 QuestionsHow do you tell a hybrid-revenue contract problem from a messy template library?

Count your template versions. More than one master template for the same revenue type is a hygiene problem. A single master template serving two or more economically distinct revenue types is a hybrid-revenue problem, and hygiene alone will not fix it. The test is whether the commercial theory of the contract matches the commercial theory of the revenue.

Who should chair a B2B contract governance council: legal, commercial, or finance?

Legal operations is the right default chair because the role requires neutrality across the three functions. A commercial chair tends to under-weight drift risk because pipeline pressure is immediate. A finance chair tends to under-weight deal velocity. A legal-ops chair with explicit authority to escalate to the CRO and CFO produces the fastest durable governance.

How do you prevent a contract governance council from becoming a committee that never decides?

Three mechanics: a written charter that defines what the council decides without escalation, a fixed quarterly calendar that does not move for pipeline pressure, and a published decision log recording every non-standard clause and variant promotion with reasons. Committees drift because their decisions are invisible. Councils hold because their decisions are on the record.

Contract governance is where pricing strategy either holds or quietly unravels. Hybrid-revenue companies: B2B2B platforms, freight, marketplaces, hardware+services, distribution: are where that unraveling happens fastest. This guide is the operator's playbook for rebuilding contract discipline when one template cannot serve three revenue types.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Michael Marn, Eric Roegner & Craig Zawada. The Price Advantage. Wiley, 2004

- Reed Holden & Mark Burton. Pricing with Confidence. Wiley, 2008

- Chris Voss & Tahl Raz. Never Split the Difference. HarperBusiness, 2016

- Roger Fisher & William Ury. Getting to Yes. Penguin Books, 1981

- Michael V. Marn & Robert L. Rosiello. Managing Price, Gaining Profit. Harvard Business Review, 1992