640bps and $19.4M EBITDA: How One PE Rollup Stopped the Bleed

How a four-company commercial-services rollup diagnosed heterogeneous discount leakage, built portco-specific guardrails instead of a single playbook, and converted recovered margin into an LP-ready EBITDA narrative. A portfolio-level operating guide, not a single-company pricing essay.

Discount Leakage Across a PE Rollup: A Portfolio-Level Operating Guide

You hold four commercial-services businesses, each a different animal, each bleeding margin in its own dialect. The fund committee wants one pricing story. The CEOs want four. The LP letter wants a number.

This paper is the middle path. How Crescent Harbor Holdings ran discount-leakage work as a portfolio discipline, without flattening four portcos into one template and without letting each run as a custom project.

TL;DR. Four portcos, four leakage shapes, one operating cadence. Shared measurement. Portco-specific guardrails. A quarterly review with three standing metrics. Year-two to year-three results: 640 basis points of combined pocket-margin recovery, $19.4M of EBITDA lift, two of four portcos cleared their 2026 LP budget targets on pricing discipline alone. Nothing required a repricing project. It required stopping the behaviors that produced the leakage.

The core problem

Crescent Harbor Holdings is a $640M AUM private equity fund in year two of a hold on a four-company commercial-services rollup. Combined portfolio revenue is $374M. Helena is the operating partner.

The four portcos:

- Cedar Freight is a regional LTL freight brokerage, $180M revenue, 410 carriers and 1,800 shippers on a B2B2B marketplace take-rate model.

- Ironsmith Parts is an industrial MRO parts distributor, $92M revenue, 46 branches, roughly 12,000 active accounts.

- Palm Coast Chemicals is a specialty chemicals wholesaler serving janitorial and hospitality buyers, $64M revenue, 3,400 accounts through 22 field reps and an online portal.

- Parcel Lane Packaging is a B2B packaging broker, $38M revenue, 180 mid-market accounts on mostly multi-year terms.

The thesis: consolidate four adjacent categories, share back-office functions, run a commercial operating model a founder-owned business could not. By the start of year two the fund committee wanted margin movement. The intuitive move was a cross-portfolio price increase. Helena declined. None of the four portcos had a credible current-price picture, and a price increase laid on top of uncharted leakage would lift the list and leave the pocket untouched. The committee backed her. That call is the reason this paper exists.

Stance one: discounting is usually a symptom. Missing guardrails, cost-to-serve invisibility, reps solving for quota under ambiguous authority, contracts aged past their useful life. Treat discount leakage as a discipline problem instead of a pricing problem, and the interventions get smaller while the results get larger.

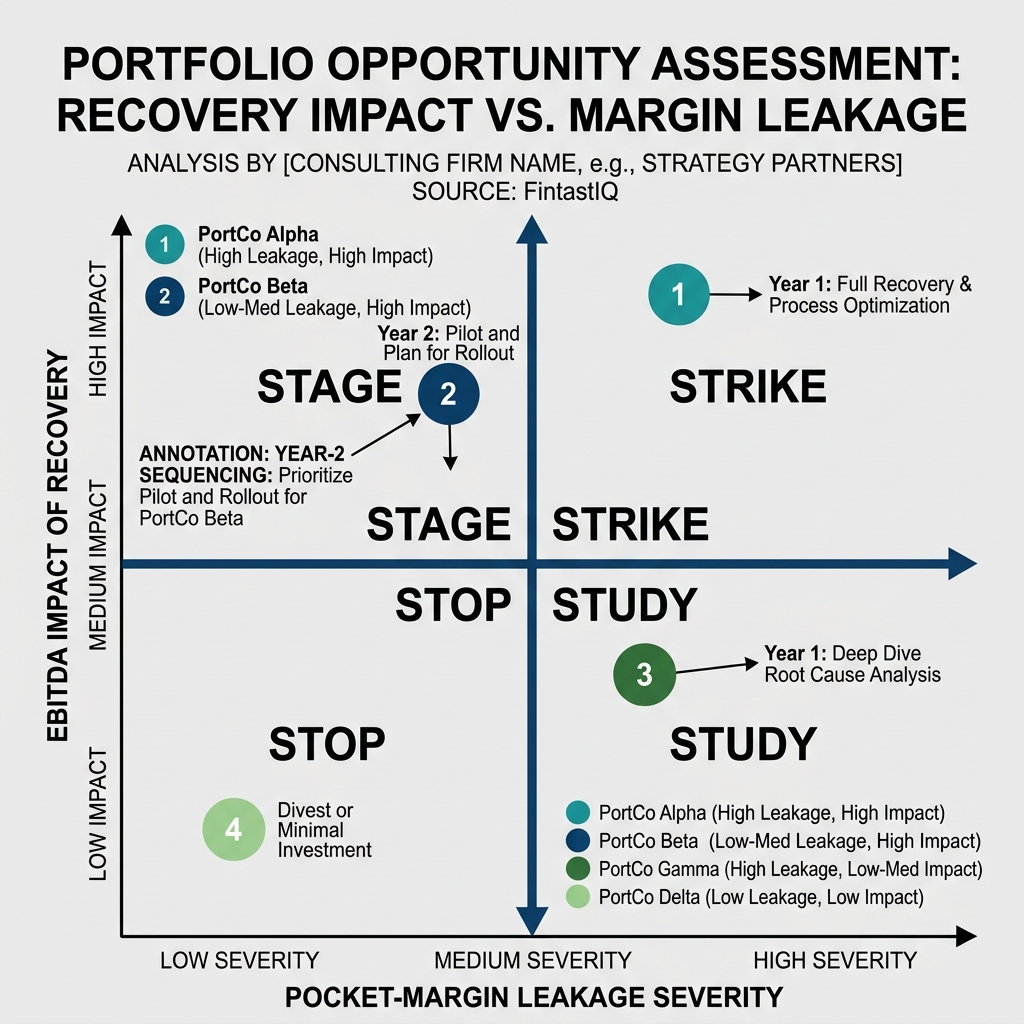

Exhibit: Portfolio-leakage quadrant chart

Exhibit: Portfolio-leakage quadrant chart

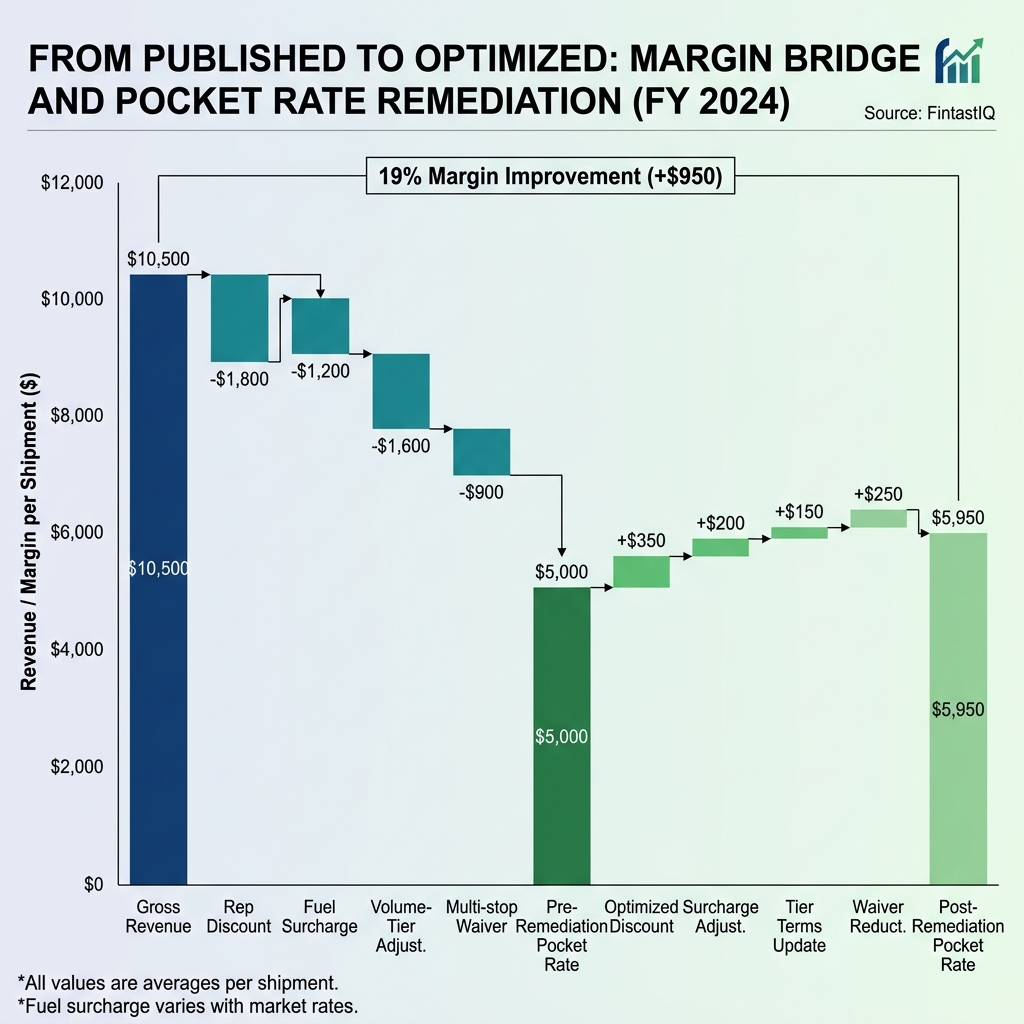

Exhibit: Cedar Freight pocket-price waterfall

Exhibit: Cedar Freight pocket-price waterfall

Part A. Diagnosing leakage across heterogeneous archetypes

A rollup diagnosis is not four single-company diagnoses stapled together. It is one measurement exercise that respects each archetype while producing a comparable view. Helena's team ran the same four steps on each business, adjusting only the reference point.

Step one: define the reference

The reference is what the portco is supposed to be charging. It looks different in each archetype.

- For Cedar Freight, the reference was the published carrier rate card and shipper tariff, measured against the pocket take-rate per lane. A B2B2B marketplace has two sides of pricing; leakage can live on either.

- For Ironsmith Parts, the reference was the system price floor loaded into the distribution ERP. Any invoice line below floor entered the leakage pool.

- For Palm Coast Chemicals, the reference was the authorized promo calendar. Anything stacked beyond the calendar was a leakage candidate.

- For Parcel Lane Packaging, the reference was contract vintage. Any account priced off an agreement more than three years old was a grandfathered candidate.

Same discipline, four reference points. You cannot run one SQL query across four businesses. You can run the same question in four dialects.

Step two: size the pool

Helena's team ran a ninety-day sample on each portco against the reference. Pre-work results:

- Cedar Freight showed 14.2% pocket-price leakage against the published rate card, concentrated in the top two hundred lanes. Rep-level discount authority was unbounded; brokers matched competitor quotes verbally and reported the match to the system after the fact.

- Ironsmith Parts showed 22% of invoice lines priced below the system floor, concentrated in twelve of forty-six branches. Branch-manager override authority was capped in theory and unbounded in practice, because the override field was free-text and rarely reviewed.

- Palm Coast Chemicals carried a case-pack promo-stacking problem costing roughly $2.4M per year in layered concessions, where reps combined catalog discount, seasonal promo, and rebate accrual on the same line.

- Parcel Lane Packaging had 31% of active contracts still priced off agreements three or more years past their original term.

Four leakage pools, four shapes, one comparable framing: how much margin is priced in before the invoice prints, and who has authority to let that happen.

Step three: attribute the leakage to a behavior

A number without a behavior cannot be fixed. Helena's team pushed every leakage pool down to a named behavior.

At Cedar Freight: verbal rate-matching on competitor quotes with no written proof. At Ironsmith Parts: branch-manager override without documented reason code. At Palm Coast Chemicals: rep-initiated promo stacking without deal-desk review. At Parcel Lane Packaging: account-manager silence at renewal on legacy accounts, because nobody wanted to be the person who raised an old price and risked the relationship.

Four behaviors. Four fixes. Zero about the list price.

Step four: lay the four on one chart

The output is a portfolio leakage quadrant. Horizontal axis: leakage size relative to portco revenue. Vertical axis: ease of intervention inside ninety days. Cedar Freight and Ironsmith Parts landed high-leakage, high-feasibility. Palm Coast Chemicals was medium on both. Parcel Lane Packaging was medium-leakage, low-feasibility because the fix waited on renewal cycles.

That chart set the sequence at Crescent Harbor Holdings: Cedar Freight and Ironsmith Parts first, Palm Coast Chemicals second, Parcel Lane Packaging as a rolling project through the renewal calendar.

Part B. Portco-specific guardrails, not one playbook copy-pasted

Stance two: the best operators compete on discipline, not instinct. Guardrails operationalize discipline. Helena's team designed four guardrail sets, one per portco, each built against the specific behavior that produced the leakage.

Cedar Freight: the verbal-match guardrail

The fix at Cedar Freight was not a new rate card. It was a written-evidence requirement. Any rate below the published card had to log against one of three reason codes: documented competitor quote with a screenshot or email, capacity-stress exception with a dispatch-timestamp, or strategic-account exception pre-authorized by the commercial lead. Anything else routed to an exception queue reviewed daily.

The broker desk hated it for three weeks. Then the published-rate realization rate moved by 380 basis points in the following quarter. On the 410-carrier side, carriers noticed the shipper quotes were holding, and Cedar Freight's willingness to walk away from unprofitable lanes improved carrier capacity commitments. The guardrail served both sides of the marketplace at once.

Ironsmith Parts: the reason-code floor

The fix at Ironsmith Parts was a structured override. The free-text ERP field was replaced with a required dropdown carrying six reason codes: competitive displacement, volume commitment above threshold, legacy grandfather match, one-time remediation, training account, and branch-discretion. The branch-discretion code was visible on every override and rolled up to a weekly branch-manager scorecard.

Below-floor invoice lines dropped from 22% to 9% in two quarters, because the reason codes made the behavior visible and the scorecard made it social. The twelve worst branches out of forty-six recovered the fastest. The disciplined branches barely moved; the ones that had been abusing override authority were now doing it in public.

Palm Coast Chemicals: the promo-stack gate

The fix at Palm Coast Chemicals was a simple arithmetic rule. No account line could carry more than two of three concession types at once: catalog discount, seasonal promo, or rebate accrual. The gate was enforced at order entry. Reps could still sell aggressively; they could not silently stack three layers on the same case pack.

That single rule recovered $1.6M of the $2.4M annual stacking loss in year one. The remaining $800K waited on the portal refresh, which added the same gate to self-serve orders.

Parcel Lane Packaging: the renewal cohort

The fix at Parcel Lane Packaging was a cohort management discipline. Every account priced off an agreement older than three years went into a named renewal cohort, sequenced across the calendar, with a price-action plan attached before the renewal conversation opened. The account manager was not raising the topic; the cohort plan was.

By month fifteen, the grandfathered-cohort share fell from 31% to 11%, and the recovered cohort repriced at an average uplift of 7.4%. The feared account-manager turnover did not materialize. Account managers preferred having the cohort plan do the talking.

Four guardrails. Four shapes. One operating logic: name the behavior, install the gate, measure the compliance.

Stance three: pricing is a signal before it is a number. Every guardrail signals what the new ownership tolerates. Before the numbers moved, the broker desk at Cedar Freight had already started quoting differently. Reputation precedes realization.

Part C. Quarterly operating review and three standing metrics

A portfolio without a cadence is a collection of projects. Helena's quarterly review carries three standing metrics, shown for every portco, every quarter, same format:

- Pocket margin versus reference. Rolling ninety-day pocket margin against the portco-specific reference. Cedar Freight uses published rate realization. Ironsmith Parts uses system-floor realization. Palm Coast Chemicals uses promo-calendar compliance. Parcel Lane Packaging uses cohort renewal uplift.

- Override rate. Percentage of transactions that cleared a guardrail exception, trailing four weeks, segmented by reason code.

- Grandfather-cohort trend. Percentage of revenue priced off a prior-era agreement.

Three numbers. Same slot. Every quarter.

Stance four: pricing maturity is measured by what you stop doing. The metrics reward cessation. Override rate falls when bad overrides stop. Grandfather-cohort trend falls when silent renewals stop. Pocket margin rises when leakage behaviors stop. It is a stop-doing review, not a do-more review.

Helena's rule: at least one portco carries yellow or red on at least one metric any given quarter. If every portco is green every quarter, the thresholds are loose or the numbers are lying.

Part D. EBITDA-to-LP narrative translation

A recovered basis point matters only when it shows up in a fund update. Helena's team writes the LP narrative around three things.

Name the behavior that stopped. LPs respond to specificity. "Cedar Freight stopped accepting verbal competitor matches without written evidence" is legible. "Pricing optimization project delivered margin lift" is not.

Quantify in basis points, not percentages. Basis points read as engineering. The combined 640 basis points of pocket-margin recovery was the number Crescent Harbor Holdings used in the year-three annual letter.

Connect to a budget target the LP already expects. Two of four portcos cleared their 2026 LP budget targets on pricing discipline alone. That framing fits the LP's existing mental model of hold-period progress without asking them to accept pricing as its own category.

End of year three: $19.4M of EBITDA lift attributable to discount-leakage work. The LP update placed that number inside the existing margin-expansion narrative, not a standalone pricing section. Pricing is a method. Margin is the story.

Three failure modes

Failure mode one: one playbook fits all

The temptation is to pick the biggest portco's playbook and spread it. The deck looks tidy. The rollout is misery. A take-rate marketplace does not respond to a distribution-floor rule. A chemicals rep network does not respond to a brokerage verbal-match guardrail. The fix is portco-specific guardrails with a comparable measurement framework above them: same pocket-margin-override-grandfather structure, same review slot, different guardrails underneath.

Failure mode two: pocket-margin focus only on the loudest portco

Cedar Freight was the biggest line and the loudest voice. Helena refused to concentrate attention there and spent roughly equal time on Palm Coast Chemicals in the first two quarters. Palm Coast Chemicals had a fast, durable fix, and shipping it early built the credibility to run the harder interventions at Cedar Freight. Winnable-fix-per-quarter equals priority.

Failure mode three: the operating review becomes theater

The colors are green, the CEOs nod, the next quarter runs. Nothing is challenged. The recovery curve flattens and nobody can explain why.

The fix is a designed challenge every review. Helena rotates the hot seat. That portco's CEO walks through three override exceptions by name, three cohort decisions by name, and one case where the guardrail produced the wrong answer and how they fixed the guardrail. Reviews that surface friction are alive.

The 30-60-90 portfolio rollout

Days 1 to 30. Align the four portco CEOs on the measurement framework: pocket-margin-versus-reference, override rate, grandfather-cohort trend. Define the reference per portco. Pull a ninety-day baseline. Name the behavior driving each leakage pool. Book the quarterly review slot for the year.

Days 31 to 60. Ship the first guardrail at the two highest-feasibility portcos. For Crescent Harbor Holdings: Cedar Freight and Ironsmith Parts. Install the exception queue, reason-code dropdown, scorecard. Hold the line for the first two weeks, because this is where programs quietly reverse.

Days 61 to 90. Begin rollout at Palm Coast Chemicals. Stand up the renewal-cohort plan at Parcel Lane Packaging. Deliver the first operating review with all four portcos plotted on the three standing metrics. Name the one portco carrying yellow or red, and the behavior that caused it.

By day ninety the program has shipped visible work at all four portcos, produced a comparable review, and made one uncomfortable disclosure. The disclosure is the proof.

FAQ

The eight-question FAQ in the frontmatter covers portco-specific guardrails, leakage archetypes, prioritization, governance ownership, review metrics, time-to-impact, CEO resistance, and LP narrative translation.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

8 QuestionsWhy does a PE rollup need portco-specific pricing guardrails instead of a shared playbook?

Because the four businesses sell to different buyers, on different contract forms, with different cost-to-serve structures. A freight brokerage earning a take-rate on 410 carriers has nothing in common with a chemicals wholesaler running case-pack promos through 22 field reps. When a single playbook is copy-pasted across portcos, it fits the loudest one and bruises the others. Guardrails work when the shape of the leakage, not the brand of the tool, drives the design.

What does pocket-price leakage actually look like across a commercial-services rollup?

It shows up as published-rate fade in freight, below-floor invoice lines in MRO distribution, stacked promo concessions in specialty chemicals, and grandfathered pricing in packaging. Each portco has its own failure shape. The common trait is that the leakage is invisible on the P&L because it is priced in before the invoice prints. You see it only by running pocket-price measurement against a published or system-of-record reference.

How does an operating partner decide which portco to fix first on pricing leakage?

Size the leakage pool, then divide by effort to fix. The portco with the widest pocket-margin gap is not automatically the first priority. If its gap is structural, for example expiring multi-year contracts, the fix takes longer than the hold period can wait. The right first move is the portco where you can install a guardrail inside ninety days and show the lift inside one quarter. That builds operating-review credibility for the harder fights.

Who owns portfolio-level pricing governance inside a PE fund: deal team or operating partner?

The operating partner, not the deal team. Deal partners own thesis; operating partners own execution. In practice a fund with a rollup thesis needs one operating partner with commercial depth who can read a pocket-price waterfall, challenge a portco CRO on override rates, and translate recovered margin into an LP update. That person does not need to be a pricing expert. They do need to trust the measurement.

Which metrics belong in a portfolio-level quarterly operating review for pricing?

Three are sufficient. Pocket margin versus a portco-specific reference, which changes shape per archetype but reads comparably across the portfolio. Override rate, meaning the percentage of transactions that cleared a guardrail exception, segmented by reason code. Grandfather-cohort trend, the share of revenue still priced off a prior-era agreement. Add a fourth only if the first three are stable and you have earned the right to complicate the conversation.

How long does it take to see EBITDA impact from portfolio-level discount-leakage work?

The first guardrails show margin lift in the quarter they ship. The full recovery curve runs twelve to eighteen months because multi-year contracts and grandfathered accounts have to roll at renewal. A realistic portfolio plan targets three to seven hundred basis points of pocket margin recovery by month eighteen, compounding toward exit. If the number comes in much faster, the guardrails are probably not holding.

What does an operating partner do when a portco CEO resists pricing guardrails?

Ask whether they object to the measurement or the limits. If it is the measurement, share the raw pocket-price sample and let them argue with the invoices. If it is the limits, ask what deal they lost this quarter because of the threshold, and show what margin was protected. Resistance is usually about loss of discretion, not about economics. The operating review metric, not the CEO vote, sets the line.

How do you write a pricing-discipline EBITDA story into an LP update without sounding promotional?

Attribute the EBITDA lift to governance, not to price increases. LPs read price increases as one-time and reversible. They read governance lift as durable and attributable to the fund, not the market. Describe what the portfolio stopped doing, quantify the pocket-margin recovery in basis points, and connect the number to a budget target the LP already expects you to hit.

How a four-company commercial-services rollup diagnosed heterogeneous discount leakage, built portco-specific guardrails instead of a single playbook, and converted recovered margin into an LP-ready EBITDA narrative. A portfolio-level operating guide, not a single-company pricing essay.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Michael Marn, Eric Roegner & Craig Zawada. The Price Advantage. Wiley, 2004

- Reed Holden & Mark Burton. Pricing with Confidence. Wiley, 2008

- William Thorndike. The Outsiders. Harvard Business Review Press, 2012

- McKinsey & Company. The Power of Pricing. McKinsey Quarterly, 2003

- Michael V. Marn & Robert L. Rosiello. Managing Price, Gaining Profit. Harvard Business Review, 1992