Why Hiring a VP Sales Before Deal 20 Costs You a Year

Founder-led sales is a phase, not a permanent condition. This guide lays out the codification sequence that turns a founder's instinct into a transferable commercial system. It maps the first twenty-four deals, the first three hires, and the three failure modes that cost early-stage operators a year of pipeline.

The Operator's Guide to Founder-Led Sales in Services and Specialty-Product Businesses

The first twenty-four deals of a specialty-product or professional-services business are not a sales process. They are a diagnostic exercise conducted on the founder's calendar. Treat them that way and the company graduates. Treat them as a precursor to a VP of sales hire and the company spends a year recovering.

This guide is written for operators whose businesses do not fit the pure SaaS template. Services firms, specialty-product companies, hardware-plus-services businesses, marketplaces with enterprise buy sides, and B2B2B arrangements. In each of these models, the founder-led phase lasts longer, the codification problem is harder, and the advice imported from velocity-SaaS writing actively misleads.

TL;DR

Founder-led sales is a phase with a defined exit sequence. The founder closes deals one through roughly twenty personally. Along the way, the founder codifies the pricing framework, the ICP, the discovery-call playbook, and the discount discipline in that order. The first account executive enters around deal twenty. A sales engineer arrives around deal twenty-eight. A second AE follows at deal thirty-two. A VP of sales conversation does not belong inside the first fifty deals. The three failure modes that cost operators the most time are hiring a VP of sales too early, building CRM workflow before the ICP is defined, and letting one or two customers negotiate free implementation. Discounting is usually a symptom. Pricing is a signal before it is a number. The best operators compete on discipline, not instinct. Pricing maturity is measured by what you stop doing.

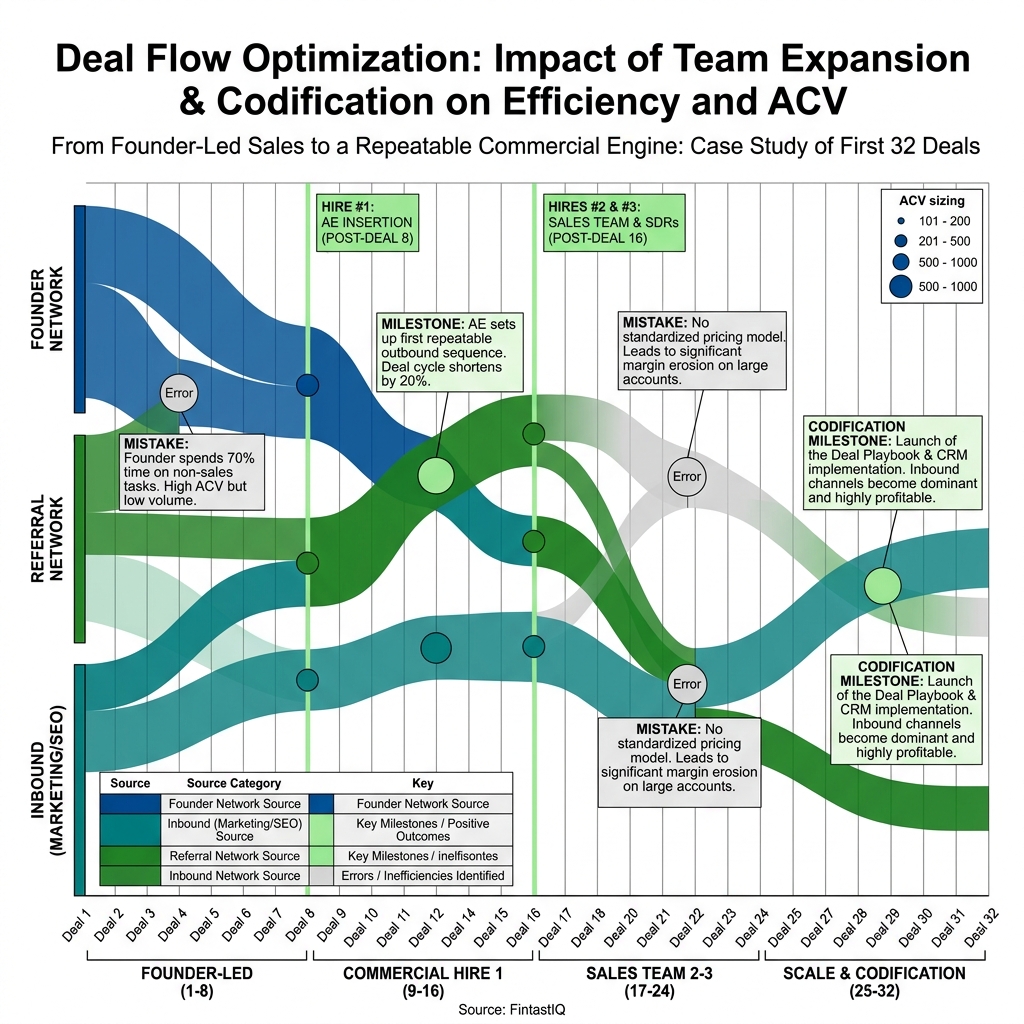

Exhibit: Founder-led deal lineage with hire-insertion timeline

Exhibit: Founder-led deal lineage with hire-insertion timeline

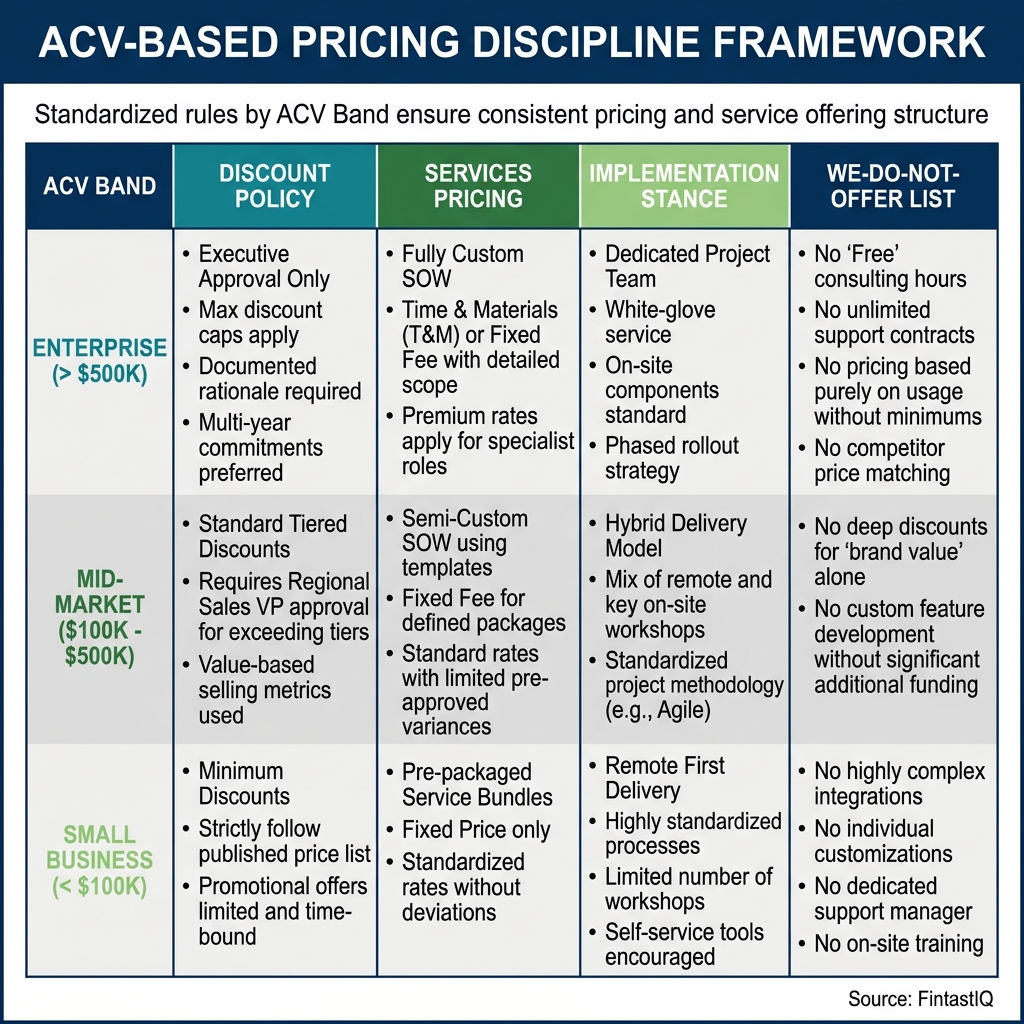

Exhibit: ACV-band pricing-discipline matrix

Exhibit: ACV-band pricing-discipline matrix

The Core Problem

Meet Quillwork and Trace. Eighteen people. Four-point-two million dollars in ARR. Twenty-four customers. Three founders: a technical founder, a commercial founder named Bríd, and a legal-domain founder. The firm sells legal-tech implementations, data migrations, and managed services to corporate legal departments. ACV ranges from eighty thousand to four hundred twenty thousand dollars. Sales cycles run ninety to one hundred eighty days. It is a specialty-product-and-services business, and the commercial operating system that fits it is specific.

Bríd personally closed deals one through twenty-four. Seventy-eight percent of first meetings were self-sourced from her network; the remaining twenty-two percent came from referral. No outbound program, no MQL funnel. A commercial founder with a rolodex, a product the market needed, and a full calendar.

That configuration is correct for the first twenty-four deals. It is also the configuration that fails if it persists past deal thirty-five.

The mistake operators make is not doing founder-led sales. The mistake is treating it as a problem to escape rather than a phase to instrument. Every hour Bríd spent in deals one through twenty generated data about the ICP, the objection set, and the price ceiling that no hired AE could have produced. The value is not the revenue. It is the calibration. Operators who skip the calibration pay for it in year two.

Four Moves That Define the Transition

(a) Why Early B2B Services and Specialty Founders Cannot Delegate Sales in Deals One Through Twenty

In a velocity-SaaS business with a two-thousand-dollar monthly ACV and a fourteen-day sales cycle, a well-hired AE can run the motion on day thirty. The sales conversation is transactional. The product is self-demonstrating. The contract is standard.

Quillwork and Trace does not work that way. An eighty-thousand-dollar implementation with a hundred-twenty-day cycle requires the seller to navigate procurement, a technical review, a security review, and three to five stakeholder conversations before a signature. The seller must answer questions on data schema mapping, redaction workflows, matter-management integration, and regulatory exposure. A founder can answer those because she built the firm around them. A hired AE on day thirty cannot.

The delegation problem is not a training problem. It is a product-depth problem. In the first twenty deals, the founder is still discovering which technical objections are disqualifying, which are negotiable, and which are mispriced. The only person with the context to run those conversations is the founder.

(b) The Codification Sequence

The sequence matters. Done out of order, the artifacts contradict each other.

The pricing framework comes first. Quillwork and Trace codified its pricing framework after deal twelve. The framework specified a day rate of four thousand eight hundred dollars, a weekly block rate of sixteen thousand dollars, and implementation bands that mapped contract size to delivery team composition. Before the framework existed, Bríd was pricing every deal from first principles. Two customers negotiated free implementation in that window, and the precedent took four subsequent deals to un-set. The framework is written in one page. Every deal since deal twelve has priced against it.

The ICP definition comes next. An ICP is not a demographic. It names the buyer, the triggering event, the budget posture, and the disqualifying conditions. Quillwork and Trace's ICP reads: general or deputy general counsel at a corporate legal department with twenty to three hundred attorneys, triggered by a matter-management migration, a regulatory event, or a shift in outside-counsel spend. Disqualifiers: legal reporting into the CFO, outside-counsel spend below three million, or an in-flight implementation with a competing vendor. The ICP fits on a note card. Deals that match it close at roughly three times the rate of deals that do not.

The discovery-call playbook follows. Quillwork and Trace codified its playbook after deal fifteen. The playbook specifies the opening frame, the five qualification questions, the objection map, the disqualification criteria, and the close sequence. It is twelve pages. Bríd wrote it by transcribing her own calls and extracting the patterns. The playbook exists so that the first AE can run the same motion on day thirty.

The discount discipline closes the loop. Quillwork and Trace does not discount on ACV below one hundred fifty thousand. The rule was founded in the pain of deal nine, where a fifteen-percent discount was granted to a customer who had no budget pressure and used the discount as a procurement trophy. Above one hundred fifty thousand, discounts are governed by a written matrix tied to contract term, implementation scope, and multi-year commitment. The matrix removes the founder's instinct from the price conversation, which is what makes the conversation transferable.

(c) The First Hires and When

The first account executive arrives at deal twenty. The candidate profile is vertical credibility, not enterprise-software pedigree. At Quillwork and Trace, the first AE had spent seven years selling into corporate legal departments at a competing vendor. She inherited a codified playbook and a functioning CRM. Her ramp was sixty days.

The sales engineer arrives at deal twenty-eight. The trigger is not a specific revenue milestone. It is the hour count on the technical-qualification calls that the founder can no longer personally absorb. The SE removes the technical founder from second and third meetings and lets the AE run a two-person motion.

The second account executive arrives at deal thirty-two. By this point, the first AE has produced enough repeatability to prove the playbook is transferable, and the pipeline is larger than one AE can cover. Hiring the second AE in parallel with the first is a known failure mode; the pattern misses the validation that a single AE on a working playbook provides.

The VP of sales conversation does not belong in the first fifty deals. Quillwork and Trace learned this the expensive way, which is the subject of the next section.

(d) The Founder's Exit-from-Deals Plan

Bríd stays deal-lead on the top eight accounts at any given moment. The qualifying criteria are written: strategic accounts that will anchor reference logos, vertical credibility, or case studies; deals above two hundred thousand in ACV; deals with a founder-level relationship that predates the company. Everything else runs through the AE pool with Bríd available for technical escalation and contract sign-off.

The exit plan is a reduction schedule, not a switch. In the month the first AE is hired, Bríd is the deal-lead on twenty-four active deals. In the following quarter, she reduces to sixteen. By the end of the second quarter after the AE's arrival, she is at the target of eight. The reduction is forced by calendar constraint: Bríd blocks the time she previously spent on deals nine through twenty-four for the work of codifying the playbook further, building the partner channel, and hiring the SE.

Founders without a written reduction schedule re-enter every deal that goes quiet. The re-entry feels like protecting the revenue. What it does is teach the AE that the founder will solve every hard problem, which prevents the AE from ever building the skill.

Three Failure Modes

The Early VP of Sales

Quillwork and Trace hired a VP of sales at deal fourteen. Strong background, enterprise legal-tech. Within six months the VP was out. The diagnosis was not the VP. The VP had nothing to manage. The playbook did not exist. The pricing framework was three weeks old. The ICP was still being refined on live calls. A VP of sales manages a commercial system. When the system does not yet exist, the VP is forced to build it from scratch while also hitting a number, and that is not a job.

The cost was not only the severance. It was nine months of founder attention diverted into a failing hire, plus the reputational drag on two candidate AEs who declined the role after the prior hire's departure became visible.

CRM Workflow Before ICP

In month ten, Quillwork and Trace built a CRM workflow with nineteen custom fields, eleven deal stages, and three separate pipelines, before the ICP was codified. Within two quarters, half the fields were unused, the stages did not match the actual buying process, and the pipelines produced reports no one trusted.

The correct sequence is ICP first, pricing framework second, discovery playbook third, CRM workflow fourth. The CRM is a reflection of the commercial process. Built before the process exists, it is a reflection of nothing.

The One Customer Who Gets Free

Two customers in the first twelve deals negotiated free implementation. Both were strategic logos Bríd wanted for reference value. The precedent took four deals to un-set. Every procurement conversation in the following six months referenced "what you did for [logo]." The cost was not the labor. It was four deals in which the pricing framework was weakened before it could harden.

The discipline is to price the strategic logo at the standard rate and, if reference value is the concern, to negotiate a reference-rights addendum instead of a discount. A logo earned at full price tells the market something a logo earned at zero does not.

30-60-90 Sprint

Days one through thirty. Audit every deal in the last twelve months. Record ACV, cycle length, source, primary objection, and close-or-loss reason. Draft the pricing framework in one page. Draft the ICP on a note card. Identify the top eight deal-lead accounts that the founder will retain after the AE hires.

Days thirty-one through sixty. Write the discovery-call playbook. Transcribe six recent founder calls and extract the opening frame, the five qualification questions, the objection map, and the close sequence. Codify the discount discipline in writing with the ACV threshold and the approval matrix. Rebuild the CRM around the new ICP and pricing framework, keeping fields to the minimum viable set.

Days sixty-one through ninety. Open the AE search. Interview against vertical credibility rather than pedigree. Prepare the thirty-day ramp plan that walks the AE through the playbook, the pricing framework, and the first five deals they will shadow. Write the founder's reduction schedule with specific deal counts by quarter.

What We Do not Share Publicly

Quillwork and Trace maintains an explicit "we do not offer" list. The list is not published. It is used internally to disqualify deals quickly and to protect the team's capacity. It includes: one-off data migrations under forty thousand dollars, litigation-support staffing, and any engagement that requires on-site presence more than two days per month. The firm has said no to an estimated two million dollars of ACV across the last twenty-four months by holding this list.

The second item not shared publicly is the internal discount matrix above the one-hundred-fifty-thousand threshold. The matrix is shared with the AE and the founder only. Publication of the matrix would create a negotiation anchor that procurement teams would use as a floor.

The third is the founder's personal deal-lead list. The top eight accounts rotate. The list is reviewed monthly. Publication would create a two-tier expectation among customers that would corrode the AE-led motion.

Exhibit One: Founder-Led Deal Lineage with Hire-Insertion Timeline

Deal # ACV Band Lead Codification Event Hire Event

-------------------------------------------------------------------------------

1-8 $80K-$180K Bríd : :

9 $120K Bríd Discount pain (15% given) :

10-11 $90K-$140K Bríd : :

12 $210K Bríd Pricing framework v1 :

13 $160K Bríd : :

14 $280K Bríd : VP Sales hired (failed)

15 $180K Bríd Discovery playbook v1 :

16-19 $100K-$320K Bríd ICP definition v1 VP Sales departs (deal 20)

20 $240K Bríd/AE-1 : First AE hired

21-27 $110K-$380K AE-1/Bríd Discount matrix v2 :

28 $340K AE-1/Bríd : Sales engineer hired

29-31 $150K-$290K AE-1/SE : :

32 $260K AE-1/AE-2 : Second AE hired

33-24* in progress AE pool : :

* Current state at the time of writing: 24 closed customers; deals 33+ in pipeline.

Exhibit Two: ACV-Band Pricing-Discipline Matrix

ACV Band Day Rate Weekly Block Discount Posture Approval

-----------------------------------------------------------------------------------

$80K - $150K $4,800/day $16,000/week No discount (0%) AE

$150K - $250K $4,800/day $16,000/week Up to 8% on term >24mo AE + Bríd

$250K - $350K $4,800/day $16,000/week Up to 12% on term >24mo Bríd

$350K - $420K $4,800/day $16,000/week Up to 15% on term +scope Bríd + technical

founder

Services day rate is the published rate. Weekly block is the published

block rate. Implementation scope is priced in team-composition tiers

(two-person, three-person, five-person) at the published day rate.

Discount matrix does not apply to services day rate below $150K ACV.

"We do not offer" list disqualifies before discount conversation begins.

FAQ

The FAQ at the top of this page addresses the eight questions Bríd is asked most often by other founders in the Quillwork and Trace band. The shortest correct answer: the sequence matters, the artifacts come before the hires, and the founder's exit is a reduction schedule rather than a decision.

A Note on Stances

Discounting is usually a symptom. Pricing is a signal before it is a number. The best operators compete on discipline, not instinct. Pricing maturity is measured by what you stop doing. These four sentences describe the operating posture that distinguishes firms that graduate from founder-led sales from firms that remain trapped in it. They are not slogans. They are tests that can be applied to any active deal and any active hire.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

8 QuestionsWhen is a founder ready to step out of first-meeting selling without collapsing pipeline?

Not before the twentieth deal in most specialty-product or professional-services businesses. Before deal twenty, the founder is still discovering which objections are real, which buyers convert, and which price points hold. A codified discovery-call playbook, a written ICP, and a pricing framework with a defensible floor are the preconditions. Without those three artifacts, a founder stepping out produces a pipeline collapse inside two quarters. The exit is a sequence, not a decision.

What is the right first sales hire for a founder-led services or specialty-product business?

An account executive with vertical credibility, not a VP of sales. A VP hired before deal twenty lacks a playbook to manage, a team to lead, and a pricing framework to enforce. An AE inherits a founder-led motion and runs it. Quillwork and Trace hired its first AE at deal twenty, once Bríd had codified discovery and pricing. The second AE came at deal thirty-two. The VP of sales conversation sits well beyond deal fifty for most firms in this band.

How should a founder price services or specialty products in the first 20 deals?

Publish the price and hold it. Quillwork and Trace uses four thousand eight hundred dollars per day or a sixteen thousand dollar weekly block for services, with no discounting on ACV below one hundred fifty thousand. A published price creates a signal before it creates a number. Buyers calibrate seriousness by the firmness of the price. Founders who discount early teach the market that the list price is a fiction, and that lesson is expensive to un-teach.

What goes inside a codified founder-led discovery-call playbook?

Five artifacts. An opening frame that states why the meeting exists. A qualification matrix covering budget holder, triggering event, and decision timeline. An objection map with the five most common objections and the exact response language. A disqualification script for when the prospect is not a fit. A close sequence that describes the next-step ask. The playbook exists so the founder stops improvising and so the first AE can execute the same motion on day thirty.

How should a founder think about discounting under $150K ACV?

Discounting is usually a symptom. It signals a value-articulation problem, a qualification problem, or a confidence problem. In every case, the cure is upstream of the price conversation. Quillwork and Trace holds a no-discount posture on ACV below one hundred fifty thousand because, at that size, a discount is almost always a substitute for better discovery. Above one hundred fifty thousand, discounting is a commercial lever governed by a written framework, not a reflex.

When should a founder hire the first sales engineer in a specialty-product firm?

When the founder is the bottleneck on technical qualification, which typically arrives between deal twenty-five and deal thirty in the Quillwork and Trace band. A sales engineer removes the founder from second and third meetings while preserving technical credibility. Hiring the SE before the AE is a common mistake. Without an AE to run the commercial motion, the SE becomes a technical-presales solo act with no pipeline to support.

What signals a premature VP of sales hire in a founder-led B2B company?

A VP hired before the founder can hand over a written playbook, a defined ICP, a pricing framework, and a functioning CRM is set up to fail. Quillwork and Trace hired a VP at deal fourteen and parted ways six months later. The diagnosis was not the VP. It was the absence of the commercial artifacts a VP is supposed to manage. A premature VP costs twelve to eighteen months of pipeline and a meaningful severance line.

How should a founder decide which deals to stay on after hiring the first AE?

Two filters. Strategic accounts that will anchor case studies, reference logos, or vertical credibility. Deals above a founder-set threshold, typically two hundred thousand dollars ACV for firms in the Quillwork and Trace band. Bríd stays deal-lead on the top eight at any given time. Everything else runs through the AE with founder support on technical escalation. The rule is written down. Founders without a written rule re-enter every deal and never exit sales.

Founder-led sales is a phase, not a permanent condition. This guide lays out the codification sequence that turns a founder's instinct into a transferable commercial system. It maps the first twenty-four deals, the first three hires, and the three failure modes that cost early-stage operators a year of pipeline.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Aaron Ross & Jason Lemkin. From Impossible to Inevitable. Wiley, 2016

- Rob Fitzpatrick. The Mom Test. Createspace, 2013

- Geoffrey Moore. Crossing the Chasm. HarperBusiness, 2014

- Matthew Dixon & Brent Adamson. The Challenger Sale. Portfolio/Penguin, 2011

- Brent Adamson, Matthew Dixon & Pat Spenner. The End of Solution Sales. Harvard Business Review, 2012