36% List-to-Pocket Leak in One Channel. Blended Hid It.

The pocket-price waterfall is the single most diagnostic exercise a multi-channel operator can run. It exposes the gap between list and realized margin at the line-item level. And it almost always reveals that the cleanest channel on the P&L is hiding the messiest discounting behavior underneath.

The Pocket-Price Waterfall: A Channel-by-Channel Diagnostic for Finding the Margin You Already Earned

The dollar you already earned

Most commercial teams do not have a pricing problem in the way they think they do. They are not mispriced on the shelf or the rate card. They have a realization problem. The dollar left the customer. It simply did not arrive.

The pocket-price waterfall is the exercise that makes the absence of arrival visible. It is a line-by-line decomposition of every deduction between the published list and the net revenue that clears after every rebate, allowance, freight absorption, co-marketing contribution, trade-spend commitment, promotional credit, and term cost. Run properly, it is the most diagnostic piece of work a multi-channel operator can do in a quarter. Run as a blended company-level average, it is one of the most misleading.

TL;DR: Build the waterfall by channel, not blended. Categorize every deduction as governed or ungoverned. Retire or restructure only what fails a specific test. Install it as a quarterly control surface. Expect 150-300 bps of margin recovery on the messiest channel and the clarity to defend every concession that remains.

Exhibit: Three-channel pocket-price waterfall

Exhibit: Three-channel pocket-price waterfall

Exhibit: Pocket-margin-by-SKU 2×2 matrix

Exhibit: Pocket-margin-by-SKU 2×2 matrix

A working example: Birchweave & Co

Birchweave & Co is a B2B branded foodservice supplier. Seventy-five people, $32M in revenue, 62 SKUs across premium coffee concentrates, flavor syrups, and dairy substitutes. The go-to-market runs three routes: 14 national restaurant-chain accounts on 24-month contracts, 8 regional distributors servicing independent operators, and a direct-to-operator e-commerce channel. Mix is 48 percent chain, 34 percent distributor, 18 percent DTC. MAP enforcement is in place. Trade-spend accruals are clean enough to pass an audit.

On paper, Birchweave looked like a disciplined mid-market specialty business. Gross margin was holding in its target band. The commercial team was performing to plan.

The head of commercial finance, Alasdair, noticed that every channel conversation at the operating table was anchored on the chain book. Distributor economics came up only when a specific distributor did. DTC was discussed almost exclusively in marketing terms. No one had ever put a single waterfall on the table that showed all three routes on the same unit basis. Alasdair built it.

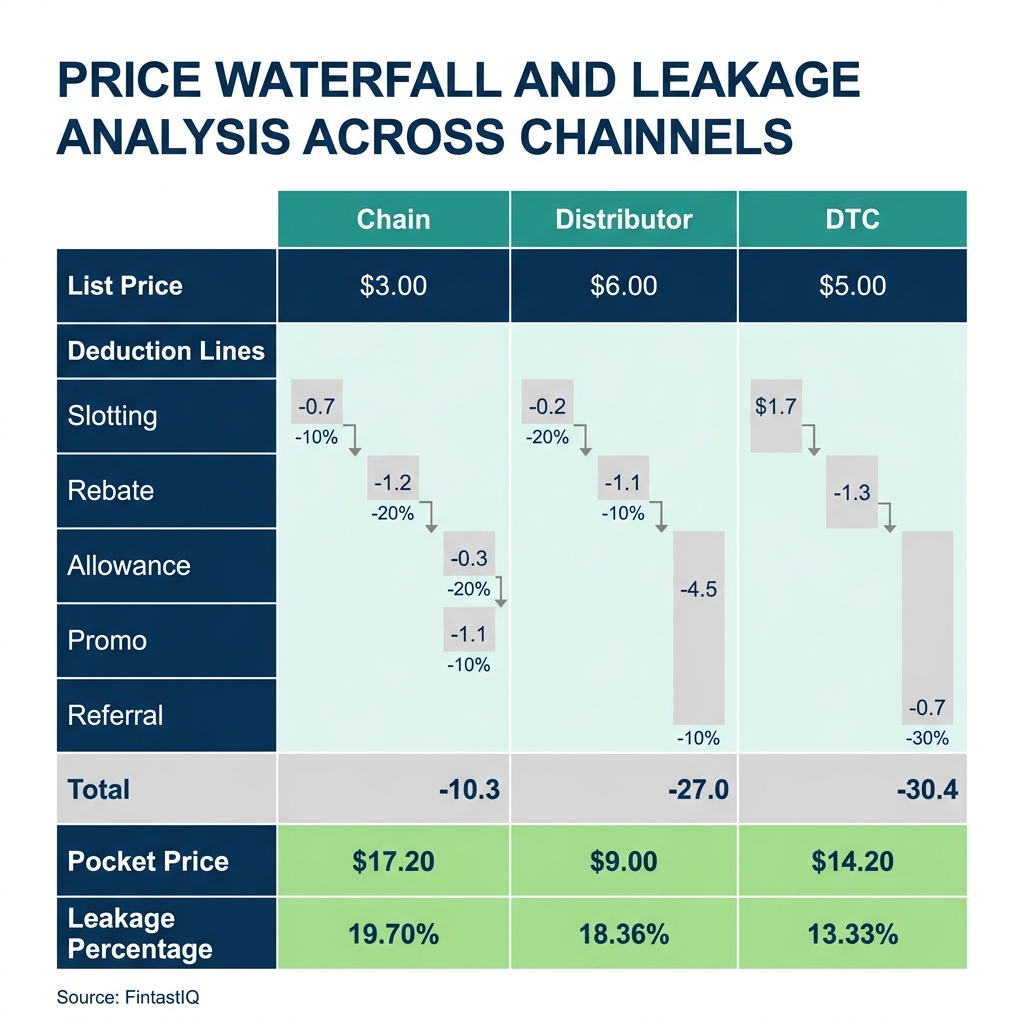

The chain waterfall started at a list price of $11.20 per unit and resolved to $7.18. The leakage was 36 percent, in five buckets: 14 percent promotional slotting, 8 percent co-marketing funds, 6 percent EDLP rebate, 5 percent freight allowance, and 3 percent menu-placement bonus. Each program had been authorized at a different time by a different commercial lead. None had been reviewed together.

The distributor waterfall started at $10.40 and resolved to $8.02. A 23 percent leakage across a 9 percent volume tier, 7 percent growth rebate, 4 percent new-door incentive, and 3 percent cash-terms discount.

The DTC waterfall started at $14.95 and resolved to $13.71. An 8 percent leakage consisting of a 5 percent first-order promo and a 3 percent referral credit. Clean, small, and known.

The chain and distributor waterfalls had never been seen in this form by the board. The DTC waterfall was, in Alasdair's phrase, "the only one that did not make me uncomfortable." The uncomfortable waterfalls are where the work is.

The four-part method

(a) Build the waterfall by channel, not blended

The first discipline is the most violated. Blended waterfalls are comfortable because they aggregate the chaos into a number the whole commercial team can live with. Channel waterfalls are uncomfortable because they force every revenue leader to see their own book without the averaging that protected them.

Build one waterfall per route to market, on a unit basis, using the same denominator. If you sell a coffee concentrate through chains, distributors, and DTC, every waterfall is built on one case of that SKU. Do not normalize to a blended unit. Do not average across pack sizes. The comparability is the point.

Start at the published list price for the channel. Subtract every deduction in sequence: contractual discounts, rebates, allowances, promotional programs, logistics absorptions, term and financing costs, and the silent concessions that appear in credit memos but were never codified in the contract. What remains is the pocket price.

This is not accounting. The waterfall is a commercial document that rearranges accounting data in the shape of a decision. Pricing is a signal before it is a number, and the waterfall is how you read the signal each channel is broadcasting about its own discipline.

(b) Categorize every line as governed or ungoverned

Every deduction falls into one of two categories. Either it was authorized by someone with the seat to authorize it, documented, capped in dollars or percentage, sunsetted, and reconcilable against a specific buyer behavior. Or it was not.

Governed concessions are fine. They may be generous, they may be renegotiable, but they are under control. You can defend them to a board.

Ungoverned concessions are the inventory of problems. A freight allowance introduced to win a single account three years ago that has since propagated to every account is ungoverned. A co-marketing fund with no campaign tied to it is ungoverned. A volume rebate paying on thresholds the customer is guaranteed to hit is ungoverned. A new-door incentive that never expires is ungoverned.

At Birchweave, the categorization flagged six ungoverned lines on the chain waterfall and four on the distributor waterfall. DTC had none. Governance collapses in the channel with the largest accounts, the longest contracts, and the most relationship-driven negotiations, because every ungoverned concession feels like a small accommodation until it is viewed beside the others.

(c) Decide what to retire and what to restructure

Discounting is usually a symptom. The task on the other side of the waterfall is not to eliminate concessions. It is to decide which ones are buying you something and which ones are not.

A line is a candidate for retirement if it meets two of the following: it has no expiry, it stacks with another program targeting the same behavior, it was authorized below the seat threshold required by policy, or its removal would not measurably change buyer behavior. A line is a candidate for restructuring if it is doing useful work but is poorly shaped, typically by lacking a sunset, a cap, or a clear performance trigger.

Birchweave retired six layered rebate lines on the chain book that stacked redundantly against the same volume behavior. Two promotional programs on the distributor book were consolidated into a single quarterly structure. One new-door incentive was rebuilt with a six-month sunset and a per-door cap, replacing what had been an open-ended program. DTC was untouched. The best operators compete on discipline, not instinct. Restructuring is how you install the discipline without abandoning the commercial relationships discounting was trying to serve.

(d) Install the quarterly pocket-price review

A waterfall run once is a diagnostic. A waterfall run quarterly is a control surface.

The review has a fixed agenda. Refresh each channel waterfall against the prior quarter. Identify every movement greater than 25 basis points, up or down, and attach a one-paragraph narrative. Flag any new concession introduced during the quarter. Reconcile governed versus ungoverned line counts. Document the dollar impact of any retirement or restructuring decisions.

The review is owned by commercial finance, chaired by the head of commercial finance, and attended by the channel commercial leaders. The CFO attends once a quarter. The board sees the summary annually. Pricing maturity is measured by what you stop doing, and the review is how you stop doing the things the waterfall keeps flagging.

Birchweave installed the review in the quarter after Alasdair's first build. By the fourth quarter, chain pocket-price was up 240 bps, distributor up 180 bps, DTC unchanged by design, and the consolidated annualized gross-margin lift was $1.1M. No list-price increases were taken. No customers were lost.

Three failure modes

Blended waterfall hides channel sins. A consolidated waterfall produces a number the whole team can tolerate. The chain team feels fine because its leakage is averaged against DTC. DTC feels fine because its volume is small. Distributor feels fine because nobody is asking sharp questions. Birchweave had this pattern for years. The remedy is mechanical: never present a pocket-price waterfall in aggregate without the per-channel breakdown sitting beside it.

The retire-everything reflex. A first waterfall typically produces a wave of embarrassment followed by a reflex to cancel every ungoverned program in the next 60 days. This is how commercial trust is destroyed in a quarter. Concessions exist because they were, at some point, buying something. The task is to determine what, not to assume nothing.

No sunset on new concessions. The most reliable predictor of whether a pricing program will become ungoverned is whether it has an end date. Programs introduced without a sunset become permanent features of the cost base within two quarters. Every new concession, without exception, should carry a sunset clause, a cap, and a named owner. If a program deserves to be extended, the renewal conversation is trivial.

The 30-60-90 install

First 30 days. Commercial finance builds the first-pass waterfall for each channel on the same unit basis. Every line item is categorized as governed or ungoverned. Circulated to commercial leadership and the CFO only. No decisions taken. The objective is a defensible, reconcilable baseline.

Days 31-60. Commercial leadership reviews the waterfalls with commercial finance and identifies retirement and restructuring candidates. Each candidate is tested against the four retirement criteria. A written decision memo is produced for each line acted upon. Customer-facing changes are sequenced to land at natural contract or program renewal points.

Days 61-90. The quarterly pocket-price review is installed as a standing cadence. The first review is held in this window with the refreshed waterfalls, the documented retirement and restructuring decisions, and the before-and-after delta. Board reporting is updated to include the channel waterfall summary. A lightweight monthly refresh is put in place for the top two channels.

Exhibit 1: The three-channel pocket-price waterfall

BIRCHWEAVE & CO: POCKET-PRICE WATERFALL BY CHANNEL (PER UNIT)

Chain Distributor DTC

List price $11.20 $10.40 $14.95

Promotional slotting (1.57) - -

Co-marketing fund (0.90) - -

EDLP rebate (0.67) - -

Freight allowance (0.56) - -

Menu-placement bonus (0.34) - -

Volume tier - (0.94) -

Growth rebate - (0.73) -

New-door incentive - (0.42) -

Cash-terms discount - (0.31) -

First-order promotional - - (0.75)

Referral credit - - (0.45)

------- ------- -------

Pocket price $7.18 $8.02 $13.71

Leakage from list 36% 23% 8%

Governed lines - 1 2

Ungoverned lines 5 3 -

Action Retire 6, Consolidate No change

restructure 1 2, rebuild

1 with sunset

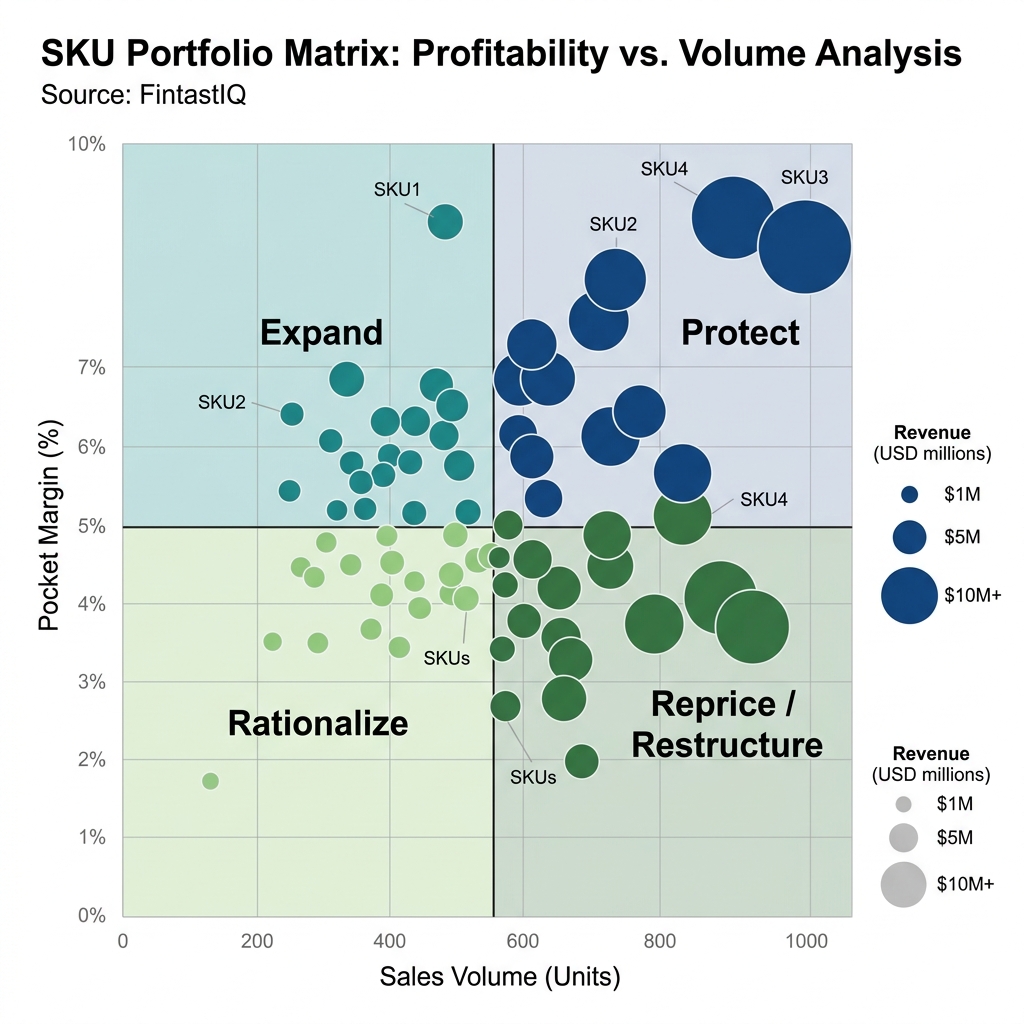

Exhibit 2: Pocket-margin-by-SKU, four-quadrant matrix

POCKET-MARGIN-BY-SKU MATRIX

(applied to all 62 SKUs)

LOW VOLUME HIGH VOLUME

+-----------------------+-----------------------+

| | |

HIGH POCKET | Q1: PROTECT | Q2: EXPAND |

MARGIN | | |

| Niche specialty | Core franchise |

| SKUs with pricing | SKUs with pricing |

| power. Guard | power AND scale. |

| carefully; these | The business runs |

| are the unit | on these. Invest |

| economics anchor. | in availability. |

| | |

+-----------------------+-----------------------+

| | |

LOW POCKET | Q3: RATIONALIZE | Q4: REPRICE OR |

MARGIN | | RESTRUCTURE |

| Low volume, low | |

| margin, often | High volume, low |

| legacy. Candidates | margin. The |

| for discontinuation | channel leakage |

| or repositioning. | lives here. Fix |

| | the waterfall |

| | before cutting. |

| | |

+-----------------------+-----------------------+

Frequently asked

What is it? A line-by-line accounting of every deduction between published list and net realized revenue. Built on invoices, credit memos, and cash. Built at the unit level for each channel.

Why by channel? Blended waterfalls average disciplined channels against chaotic ones. The Birchweave chain book was leaking 36 percent and the blended figure had never surfaced it.

How is this different from a discount report? A discount report shows intent. Trade-spend review shows accrual. A pocket-price waterfall shows what happened to the dollar against the unit that shipped.

Who owns it? Commercial finance on mechanics, commercial leadership on decisions.

How often? Quarterly full refresh, monthly lightweight on top channels.

What should a board see? Per-channel waterfall, governed-versus-ungoverned map, quarterly narrative for every swing above 25 bps.

Typical gains? 150-300 bps on the messiest channel in two quarters. Birchweave delivered 240 and 180 on chain and distributor, worth $1.1M annualized.

How do you avoid over-correcting? Retire only what fails a defined test. Restructure what is doing useful work but shaped poorly. Leave alone what is already disciplined.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

8 QuestionsWhat exactly is a pocket-price waterfall and what does it measure?

A pocket-price waterfall is a line-by-line accounting of every deduction that sits between the price on your published list and the net revenue that clears after all rebates, allowances, freight absorptions, co-marketing funds, promotional credits, and term costs. The outputs are not estimates. They are reconciled to invoices, credit memos, and bank activity. A proper waterfall is built at the unit level for each channel, not blended, because blending hides the channel where discipline has quietly collapsed.

Why build the pocket-price waterfall by channel rather than blended at the company level?

Because channels behave differently, are governed by different contracts, and carry different leakage archetypes. A blended waterfall averages a disciplined DTC book against a chaotic chain-account book and produces a number that looks acceptable while concealing the real problem. When Alasdair at Birchweave & Co separated chain, distributor, and direct-to-operator waterfalls, the chain channel was leaking 36 percent from list to pocket. The blended figure had never triggered a board conversation.

How is a pocket-price waterfall different from a discount report or trade-spend review?

A discount report shows what you intended to give away. A trade-spend review shows what the finance team has accrued. A pocket-price waterfall shows what actually happened to the dollar, line by line, against the unit that left the warehouse. It captures the discounts nobody authorized, the rebates that stacked, and the allowances that never expired. It is the operating reality, not the accounting reality.

Who should own the pocket-price waterfall: revenue, finance, or commercial finance?

Commercial finance should own the mechanics. Commercial leadership owns the decisions that flow from it. The worst configuration is when revenue owns the waterfall, because revenue is accountable to the top line and will under-report concessions that look embarrassing. The second-worst configuration is when finance owns it in isolation, because finance lacks the commercial context to distinguish a bad discount from a strategic investment. The head of commercial finance, sitting between the two, is the right seat.

How often should a pocket-price waterfall be refreshed to stay diagnostic?

Quarterly at minimum, with a lightweight monthly refresh on the top ten accounts or top two channels. The diagnostic value degrades fast once discounting patterns shift, and most commercial teams introduce new concession structures on a monthly cadence. A waterfall that is older than a quarter is a historical artifact. A live one is a control surface.

What gross-margin gains do operators see from a first-pass pocket-price waterfall?

In our practice, a first-pass waterfall typically recovers 150 to 300 basis points of gross margin on the messiest channel within two quarters. Birchweave recovered 240 bps on its chain book and 180 bps on its distributor book, combining to $1.1M of annualized margin. The DTC book was already disciplined and moved by design. Second-order gains, from retiring stacked programs and installing sunset clauses, typically add another 50 to 100 basis points over the following year.

How do you avoid the trap of retiring every concession program that looks messy?

You do not retire programs because they are messy. You retire or restructure them because they fail a specific test: the concession does not change buyer behavior, it has no expiry, it stacks with another program, or it was authorized by someone without the seat to approve it. A program that is ugly but is genuinely buying you shelf, velocity, or channel access stays. The retire-everything reflex destroys more value than it creates and burns commercial trust you will need for the harder conversations.

What should a board see from pocket-price waterfall work each quarter?

Three artifacts. A waterfall by channel showing list-to-pocket at the unit level. A rebate and allowance map showing which programs are governed, which are ungoverned, and which have no sunset. A quarterly pocket-price review document showing movement versus the prior quarter with a short narrative explaining every swing greater than 25 basis points. That is the full commercial-finance operating rhythm. If the board is seeing anything less, they are seeing accounting, not commercial truth.

The pocket-price waterfall is the single most diagnostic exercise a multi-channel operator can run. It exposes the gap between list and realized margin at the line-item level. And it almost always reveals that the cleanest channel on the P&L is hiding the messiest discounting behavior underneath.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Michael Marn, Eric Roegner & Craig Zawada. The Price Advantage. Wiley, 2004

- John L. Daly. Pricing for Profitability. Wiley, 2002

- Ron Baker. Pricing on Purpose. Wiley, 2006

- Michael V. Marn & Robert L. Rosiello. Managing Price, Gaining Profit. Harvard Business Review, 1992

- McKinsey & Company. The Power of Pricing. McKinsey Quarterly, 2003