Value Based Pricing: The Discipline That Anchors WTP, Not Cost

Value-based pricing treats price as a function of customer-realized value, not internal cost. This guide translates that principle into three discovery methods and a price architecture for each commercial archetype. It closes with a 30-60-90 sprint an operator can run without a consultant in the room.

The Operator's Guide to Value-Based Pricing

Most pricing conversations start with the cost sheet. That is the first mistake. The second is treating the competitor's price as a ceiling rather than a choice that competitor made with the evidence they had. Value-based pricing says the only durable anchor is the buyer's perception of worth, and the operator's job is to discover that number.

TL;DR

- Value-based pricing is a discipline, not a slogan. Price reflects customer-realized value, and the operator builds the evidence that sizes it.

- Three discovery methods cover most situations: structured willingness-to-pay interviews, choice-based conjoint, and a Van Westendorp plus Gabor-Granger composite for price sensitivity.

- The output is a price architecture, not a price point. Architecture covers headline price, packaging tiers, attach items, channel terms, and discount guardrails.

- Commercial archetype shapes the translation. DTC, specialty wholesale, B2B restaurant supply, marketplaces, and professional services each demand a different price structure even when the underlying value logic is identical.

- A 30-60-90 sprint is enough to produce a first defensible price architecture if the operator holds the line on sequence and evidence.

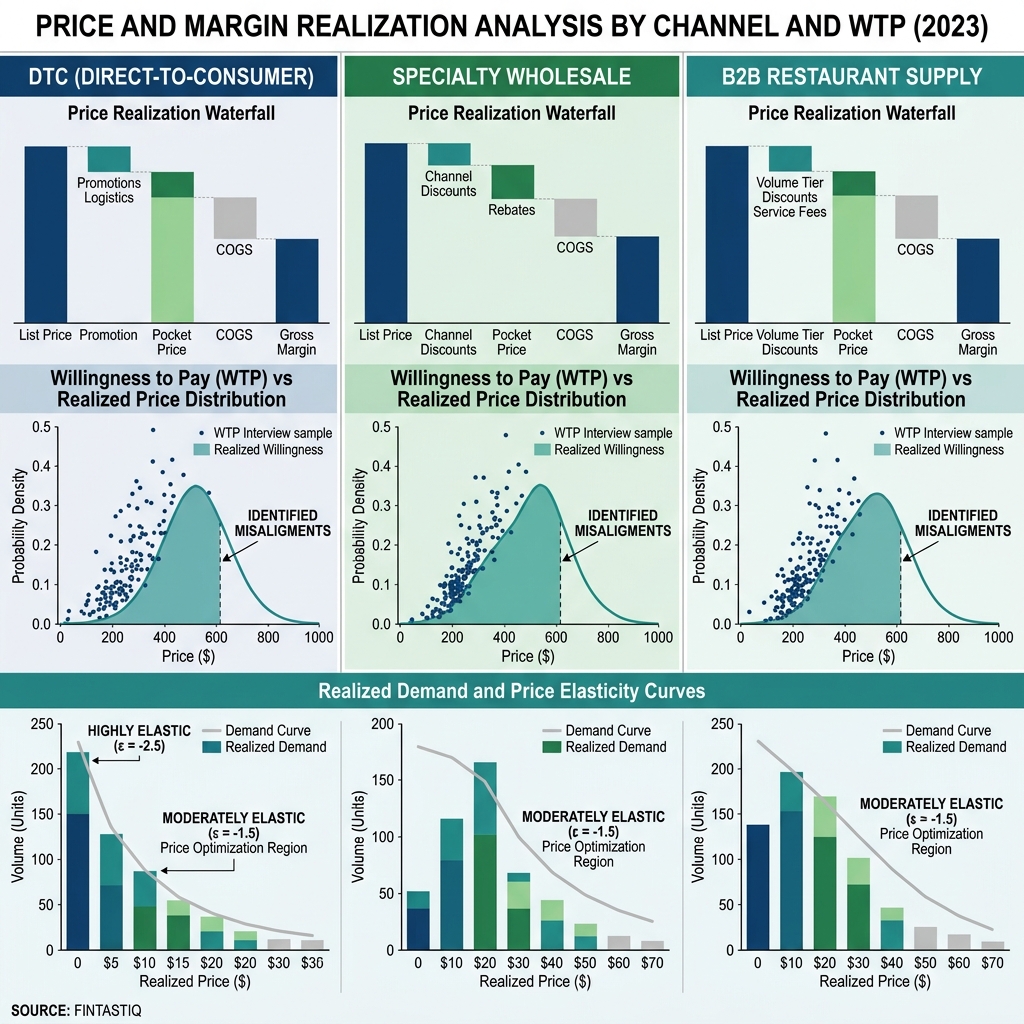

Exhibit: Channel-margin composite chart

Exhibit: Channel-margin composite chart

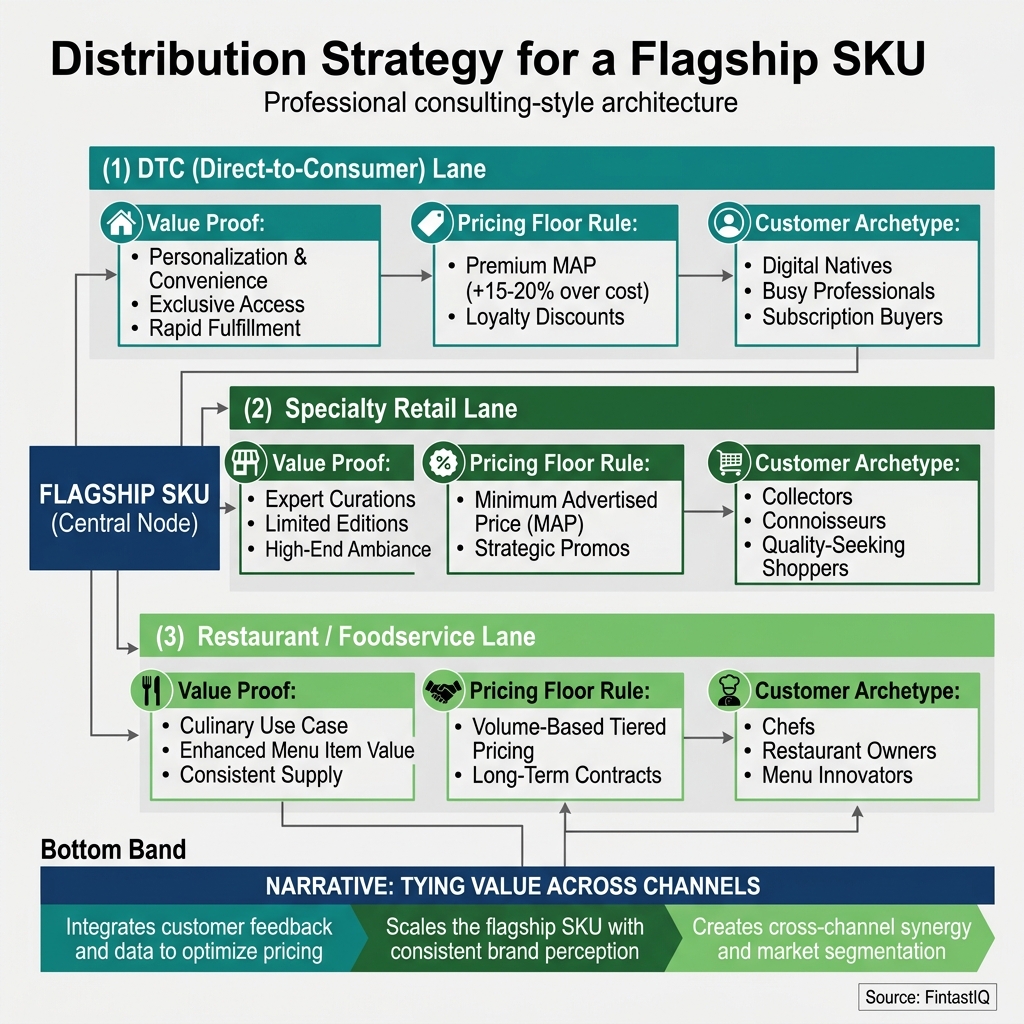

Exhibit: Cross-channel value architecture

Exhibit: Cross-channel value architecture

The core problem: price as signal before number

Kiln & Cove Outdoors is a premium outdoor cookware brand with 70 people and $28M in revenue. The channel mix is 52 percent direct-to-consumer, 32 percent specialty wholesale through 180 independent kitchenware retailers, and 16 percent B2B restaurant supply where Kiln & Cove acts as house-labeled stock for 3 premium restaurant groups. Gross margin tells the story the P&L cannot on its own: 64 percent in DTC, 38 percent in specialty wholesale, 22 percent in restaurant supply. The flagship carbon-steel pan sells for $195 against an incumbent priced at $79.

When Sona took the CEO seat, the pricing conversation was stuck. DTC traffic converted at a rate the team thought was low. Specialty buyers pushed back on the seasonal price list. The restaurant supply accounts treated Kiln & Cove as a commodity at negotiated tiers. Each channel had a different symptom, and each team had a different theory. The shared root cause was that no one had asked buyers what the product was worth to them, so every internal debate defaulted to cost and competitor price. That is the condition value-based pricing is built to escape.

The reframe Sona chose was to treat price as a signal first and a number second. A $195 pan next to a $79 pan is a claim about the product, the buyer, and the occasion. If the claim is backed by evidence of value and a packaging structure that matches how buyers actually shop, the price holds. If the claim is unsupported, any price is fragile. Packaging beats pricing, and confusion is the enemy of willingness to pay.

Part one: define customer value in your archetype's language

Value is not a single quantity. It is an outcome stated in the buyer's own words, converted into a unit the operator can measure. The first work of a value-based pricing process is to write the value definition for each segment in each channel, using language a buyer would recognize.

For the DTC consumer buying a Kiln & Cove pan, value shows up as cooking results, durability across years of use, and the emotional signal of owning a serious piece of kit. Each of those can be framed in units: number of household-level cooking occasions the pan handles, expected replacement interval against alternatives, rating the buyer gives the cooking outcome on their own scale. These are not abstractions. In 11 willingness-to-pay interviews with Kiln & Cove DTC buyers, the value language clustered around three phrases: "pans that earn a spot on the wall," "kit that survives my kids," and "food that tastes the way I wanted it to." The operator's job is to hear those and convert them into what the buyer would pay for the guarantee.

For the specialty wholesale buyer, the value language shifts. The buyer is a store owner who needs the product to sell through at a defensible margin, bring customers back, and justify the shelf space in a small footprint. Value is inventory turns, basket size lift, and lower return rates. A product that carries those outcomes can support the wholesale terms that deliver 38 percent margin to Kiln & Cove while protecting store margin.

For the B2B restaurant supply buyer, value is operational. The chef cares about consistent performance across stations, replacement cost when pans are abused in service, and the cleaning protocol the kitchen can sustain. Value is stated in service-hours saved, replacement cycles avoided, and variance reduced on the line. A 22 percent gross margin here is not a failure, it is a calibration, so long as the volume and strategic signal are worth it.

The discipline is to write these definitions down in the buyer's words, not the brand's words. Pricing is a signal before it is a number, and the signal must land in the language the buyer already speaks.

Part two: choose the value-discovery method that fits your commercial motion

Three methods cover most operator situations. The choice among them should reflect what decision the pricing work needs to support.

Structured willingness-to-pay interviews are the right starting point when the product is differentiated, the buyer population is reachable, and the pricing question is open. A willingness-to-pay interview is not a customer-discovery chat. It uses a fixed protocol that walks the buyer through the problem, the alternatives they currently use, their reference prices, and a laddered set of hypothetical prices for specific configurations. The goal is to emerge with a distribution of acceptance points and the reasoning behind each one. For Kiln & Cove, 11 interviews across DTC buyers surfaced a willingness-to-pay band for the flagship pan that sat well above the starting price and gave the team the language for the launch page.

Choice-based conjoint is the right method when the offer has multiple attributes that interact. Size, material, handle type, warranty length, bundle composition, and price can be tested together. Each respondent makes a series of forced choices between product configurations, and the analysis produces part-worth utilities that show how much each attribute drives preference. A six-cell conjoint for Kiln & Cove tested three pan sizes against two warranty options across three price points. The result told the team which bundle combinations were most preferred and at what price band each bundle lost share to the incumbent. Six conjoint cells are enough to steer packaging decisions if the cells are chosen well.

Van Westendorp combined with Gabor-Granger is a price sensitivity method for a known product at varying price points. Van Westendorp asks four price questions, and the intersections of the resulting curves define a range of acceptable prices and the optimal price point. Gabor-Granger walks each respondent up and down a price ladder to find the individual acceptance point. Running them together produces a composite chart that shows both the population-level range and the individual distribution. This is the fastest method when the product is defined and the question is where to set the number.

The one-method dogmatism failure mode shows up when an operator picks a method and runs it for every question. The better pattern is to match method to decision and sequence them: interviews to define value and segments, conjoint to design the offer, Van Westendorp and Gabor-Granger to tune the price band before launch.

Part three: translate value into a price architecture, not a price point

A price architecture covers five elements: the headline price on the hero item, the packaging tiers that frame it, the attach items that travel with it, the channel terms that carry it to market, and the discount guardrails that protect it. The operator who produces a number without the other four elements has done one fifth of the work. Packaging beats pricing because a coherent architecture can lift blended price without a single headline increase.

In the software archetype, the architecture is seats and usage. Seats carry the headline price, usage tiers carry expansion, and enterprise add-ons carry the premium edge. The discipline is to align the metric to the customer's value driver and to avoid packaging that forces buyers into tiers they do not need.

In the consumer durable archetype that Kiln & Cove occupies, the architecture is hero pricing, good-better-best within a product family, and accessory attach. A flagship pan at $195 is a premium anchor. A starter pan at $115 gives the hesitant buyer a way in. A matched set at $340 gives the confident buyer a way to commit. Each step in the architecture signals a different use case and protects the headline number. Kiln & Cove lifted flagship price by 14 percent after the study because the architecture absorbed the rise without pushing buyers out of the brand.

In the marketplace archetype, the architecture is take-rate tiering by seller size or category, plus optional service layers like ads, fulfillment, and payments. The value question is what the marketplace delivers to the seller per unit of GMV, and the tiering should reward the behaviors the marketplace wants to encourage.

In the hardware plus consumables archetype, the architecture is an anchored device price paired with consumables, service, and warranty that carry the lifetime value. The device can even run at thin margin if the consumables stream is structured to deliver the cumulative value share the operator needs.

In the professional services archetype, the architecture is value fees structured around outcomes, milestones, or retainers, with a clear definition of scope and a separate pricing path for out-of-scope work. Hourly billing is the cost-plus default and should be used only where outcomes cannot be specified.

Kiln & Cove built a cross-channel price architecture that held the DTC flagship at $195, set specialty wholesale terms that protected the retailer's margin while delivering 38 percent to Kiln & Cove, and held the restaurant supply price at the 22 percent margin level with a defined volume commitment and a separate price for custom finishes. One product, three architectures, one value logic.

Part four: instrument willingness-to-pay evidence post-launch

Value evidence is not a one-time artifact. It decays as the market moves, as the product changes, and as the buyer base evolves. An operator who treats the pre-launch study as the last word is running on stale data within twelve months.

The instrumentation has three layers. First, a light quarterly pulse that tracks conversion rate by price point, discount depth by channel, and stated reasons for loss in DTC checkout exit surveys and wholesale account reviews. Kiln & Cove saw demo-to-purchase conversion lift by 29 percent in DTC after the new architecture launched, and the team used that metric as the primary indicator that the price signal was landing. The 18 percent repeat purchase within 90 days told them the product was delivering the value the price had promised.

Second, a semi-annual deep review that refreshes two or three of the willingness-to-pay cells from the original study and adds one new segment or product cell. The goal is to watch the distribution move, not to rerun the entire study.

Third, a trigger list. Input cost movement above five percent, a competitor repricing, a new channel launch, a significant product change, or a shift in buyer composition triggers an out-of-cycle review. Kiln & Cove lost zero wholesale accounts on the price rise in part because the review cadence caught each retailer's specific concern and addressed it in channel terms rather than headline price.

The best operators compete on discipline, not instinct. Instrumentation turns pricing from a seasonal debate into a standing rhythm.

Three failure modes

Cost-plus disguised as value-based

The most common failure mode is a team that says value-based and does cost-plus. The tell is sequence. The team starts with landed cost, adds a margin target, reasons to a number, then writes a value story to justify it. The fix is to run the process in the other order and to enforce the rule that if the value-discovery output does not clear margin, the response is to redesign packaging or cost structure, not to quietly raise the cost-plus markup. Sona audited Kiln & Cove's pricing deck and found two products where the value story had been retrofitted. Both were repackaged rather than reprice-justified.

One-method dogmatism

The second failure mode is attachment to a single method. Teams fall in love with conjoint and run it for questions that Van Westendorp would answer in a week. Or they run willingness-to-pay interviews and skip the quantitative step, then launch on a sample of eleven when the decision warranted two hundred. The fix is to match method to decision, and to sequence methods so each builds on the last.

Value-based pricing without packaging

The third failure mode is the operator who sets a defensible price on the hero item and ships it without the surrounding architecture. The good-better-best is missing, the attach items are ad hoc, the discount guardrails are informal. Blended price underperforms, not because the headline number is wrong but because the structure around it never formed. Packaging beats pricing, and a lonely hero price is a packaging gap.

The 30-60-90 sprint

Days 1 to 30 are for value definition and method choice. Write the value language for each segment in each channel in the buyer's own words. Decide which decision the pricing work must support, and choose the method mix. Schedule eight to fifteen interviews per segment, or a conjoint with cells matched to the top attribute questions, or a Van Westendorp plus Gabor-Granger field with a defined sample.

Days 31 to 60 are for evidence and architecture design. Run the study. Analyze the results. Draft the price architecture for each channel, covering hero pricing, packaging tiers, attach items, channel terms, and discount guardrails. Pressure-test the architecture against at least two internal skeptics and one external advisor before it touches buyers.

Days 61 to 90 are for phased rollout and instrumentation. Launch to one channel or one segment first if reversibility is a concern. Instrument the pulse metrics from day one. Run a post-launch review at day 80 to confirm the architecture is performing as the study predicted, and schedule the first semi-annual deep review before closing the sprint.

What we do not share publicly

We keep a set of sample willingness-to-pay protocols, conjoint cell designs, and pricing architectures off the public site because the specific wording and structure are part of how our clients win. Operators who engage us see the full versions, including the question bank for interviews, the cell-design worksheet, the composite chart template, and the channel-term playbook we use when a single product has to hold three different margins without losing its value signal.

Frequently asked questions

What is value-based pricing in plain terms?

Value-based pricing sets the price of a product or service based on what the customer gains from using it, measured in money, time, or emotional payoff. Cost of production, competitor prices, and historical pricing become inputs, not anchors. The operator asks what buyers would pay if they understood the benefit fully, then builds a price and a packaging structure that captures a fair share of that value. It applies to software, physical goods, marketplaces, and services with equal force.

Does value-based pricing only work for premium brands?

No. Value-based pricing works for any brand that can describe a measurable outcome a customer cares about. A budget-tier pressure cooker brand can price on time saved per week. A mid-market payroll service can price on audit risk avoided. A luxury cookware brand can price on longevity and cooking performance. The method scales to the segment. What changes is the value metric, the willingness-to-pay band, and the packaging, not the underlying discipline.

How is willingness-to-pay research different from a focus group?

A focus group asks what people think. Willingness-to-pay research asks what people would pay, under which conditions, for which configuration. The questions are structured, the stimuli are controlled, and the analysis produces numeric distributions rather than quotes. Good willingness-to-pay research uses trade-off tasks, price laddering, or reference-product comparisons. It often combines qualitative interviews with a quantitative instrument so the operator hears the reasoning and sees the curve.

When should we use choice-based conjoint versus Van Westendorp?

Choice-based conjoint is right when the product has multiple features that interact, such as size, material, warranty, and price. It gives you part-worth utilities and lets you simulate demand for specific bundles. Van Westendorp is a price sensitivity tool for a known product at varying price levels. Use conjoint to design the offer. Use Van Westendorp to pressure-test the price band. Gabor-Granger sits between them, laddering a single product across price points to find acceptance curves.

What sample size do we need for credible willingness-to-pay work?

For qualitative willingness-to-pay interviews, eight to fifteen conversations per segment usually surface the decision logic. For a choice-based conjoint among consumers, aim for 200 to 400 respondents per segment to stabilize part-worths. For B2B buyer conjoint, 60 to 120 qualified respondents is often enough if the segment is tight. Van Westendorp needs 150 to 300 respondents per segment to produce clean intersection points. Smaller samples still inform decisions if the operator treats outputs as directional.

How do we avoid cost-plus pricing disguised as value-based?

The tell is the sequence. If the team starts with landed cost, adds a margin target, then reasons backwards to a value story, the pricing is cost-plus with a value wrapper. A genuine value-based process starts with the customer outcome, sizes willingness to pay, designs packaging to match buyer segments, then checks that the resulting price clears required margin. If margin is short, the fix is packaging redesign or cost engineering, not quiet upward revision of the cost-plus markup.

How often should we revisit pricing?

Pricing is a standing operating rhythm, not a project. A light quarterly review checks win rates, discount depth, and stated reasons for loss. A deeper annual review refreshes willingness-to-pay evidence and tests packaging hypotheses. Major product changes, channel expansion, input-cost shifts above five percent, or a competitor repositioning should trigger an out-of-cycle review. The operators who treat pricing as a muscle, not an event, compound margin faster than peers who wait for pain.

What is the fastest way to see a pricing lift without risking volume?

Start with packaging. A well-structured good-better-best or a clear attach-rate play around consumables and services often lifts blended price without any headline increase. Next, trim the discount stack. Many operators lose three to eight points of margin to layered discounts that no one has audited in a year. Only after those are in hand should you adjust the headline price on the hero item, and only with willingness-to-pay evidence and a reversibility plan ready.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

8 QuestionsWhat is value based pricing in plain operator terms?

Value-based pricing sets the price of a product or service based on what the customer gains from using it, measured in money, time, or emotional payoff. Cost of production, competitor prices, and historical pricing become inputs, not anchors. The operator asks what buyers would pay if they understood the benefit fully, then builds a price and a packaging structure that captures a fair share of that value. It applies to software, physical goods, marketplaces, and services with equal force.

Does value based pricing only work for premium brands?

No. Value-based pricing works for any brand that can describe a measurable outcome a customer cares about. A budget-tier pressure cooker brand can price on time saved per week. A mid-market payroll service can price on audit risk avoided. A luxury cookware brand can price on longevity and cooking performance. The method scales to the segment. What changes is the value metric, the willingness-to-pay band, and the packaging, not the underlying discipline.

How is willingness-to-pay research different from a customer focus group?

A focus group asks what people think. Willingness-to-pay research asks what people would pay, under which conditions, for which configuration. The questions are structured, the stimuli are controlled, and the analysis produces numeric distributions rather than quotes. Good willingness-to-pay research uses trade-off tasks, price laddering, or reference-product comparisons. It often combines qualitative interviews with a quantitative instrument so the operator hears the reasoning and sees the curve.

When should you use choice-based conjoint versus Van Westendorp price sensitivity?

Choice-based conjoint is right when the product has multiple features that interact, such as size, material, warranty, and price. It gives you part-worth utilities and lets you simulate demand for specific bundles. Van Westendorp is a price sensitivity tool for a known product at varying price levels. Use conjoint to design the offer. Use Van Westendorp to pressure-test the price band. Gabor-Granger sits between them, laddering a single product across price points to find acceptance curves.

What sample size do you need for credible willingness-to-pay research?

For qualitative willingness-to-pay interviews, eight to fifteen conversations per segment usually surface the decision logic. For a choice-based conjoint among consumers, aim for 200 to 400 respondents per segment to stabilize part-worths. For B2B buyer conjoint, 60 to 120 qualified respondents is often enough if the segment is tight. Van Westendorp needs 150 to 300 respondents per segment to produce clean intersection points. Smaller samples still inform decisions if the operator treats outputs as directional.

How do you avoid cost-plus pricing disguised as value based pricing?

The tell is the sequence. If the team starts with landed cost, adds a margin target, then reasons backwards to a value story, the pricing is cost-plus with a value wrapper. A genuine value-based process starts with the customer outcome, sizes willingness to pay, designs packaging to match buyer segments, then checks that the resulting price clears required margin. If margin is short, the fix is packaging redesign or cost engineering, not quiet upward revision of the cost-plus markup.

How often should an operator revisit pricing as a standing rhythm?

Pricing is a standing operating rhythm, not a project. A light quarterly review checks win rates, discount depth, and stated reasons for loss. A deeper annual review refreshes willingness-to-pay evidence and tests packaging hypotheses. Major product changes, channel expansion, input-cost shifts above five percent, or a competitor repositioning should trigger an out-of-cycle review. The operators who treat pricing as a muscle, not an event, compound margin faster than peers who wait for pain.

What's the fastest way to lift price without risking volume?

Start with packaging. A well-structured good-better-best or a clear attach-rate play around consumables and services often lifts blended price without any headline increase. Next, trim the discount stack. Many operators lose three to eight points of margin to layered discounts that no one has audited in a year. Only after those are in hand should you adjust the headline price on the hero item, and only with willingness-to-pay evidence and a reversibility plan ready.

Value-based pricing treats price as a function of customer-realized value, not internal cost. This guide translates that principle into three discovery methods and a price architecture for each commercial archetype. It closes with a 30-60-90 sprint an operator can run without a consultant in the room.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Hermann Simon. Confessions of the Pricing Man. Springer, 2015

- Madhavan Ramaswamy & Georg Tacke. Monetizing Innovation. Wiley, 2016

- Michael Marn, Eric Roegner & Craig Zawada. The Price Advantage. Wiley, 2004

- Thomas Nagle & Georg Müller. The Strategy and Tactics of Pricing. Routledge, 2016

- Michael V. Marn & Robert L. Rosiello. Managing Price, Gaining Profit. Harvard Business Review, 1992

- Rafi Mohammed. The Good-Better-Best Approach to Pricing. Harvard Business Review, 2018