Every Feature Decision Is a Pricing Decision. Stop Pretending.

Every feature decision is a pricing decision, whether your operating model admits it or not. Most product and pricing teams run parallel calendars, trade artifacts at the end, and ship features that never earn what the roadmap promised. The discipline is a four-part integration: classify every feature by packaging role, gate it inside a pricing-integrated ceremony before engineering commits, feed the decision into the meter-and-package map, and close the loop with post-launch revenue instrumentation. Packaging beats pricing. Pricing is a signal before it is a number.

The Operator's Guide to Product-Pricing Integration

Every feature decision is a pricing decision. Your operating model either admits that or it pays for pretending otherwise.

Most product and pricing teams run on parallel calendars. Product ships. Pricing reacts. The pricing page gets rewritten the quarter after the feature lands, by which point the meter is wrong, the package is already confusing, and the buyers who saw the feature first have anchored on the wrong number. The loss shows up as compressed take-rates, tier mix skewed to the cheapest option, and a roadmap that keeps producing features the commercial team cannot sell at the price the pricing team modeled.

Integration is not a meeting. It is a discipline with four parts.

TL;DR.

- Every feature is a packaging-power bet, a value-driver bet, a defensive must-have, or a no-monetization-thesis item. If you have not classified it, you have not priced it.

- The pricing-integrated decision gate is one ceremony, on the calendar, where product, pricing, finance, and a frontline seller sign on an artifact before engineering commits. No gate, no build.

- The meter-and-package map is the connective tissue. Every feature decision must name the meter it feeds and the tier it lives in. Hybrid models (hardware plus software plus marketplace) need this more, not less.

- Close the loop with post-launch instrumentation. If the revenue hypothesis misses by 40 percent at day 90, the feature re-enters the gate. Pricing maturity is measured by what you stop doing.

- Packaging beats pricing. Confusion is the enemy of willingness to pay. The best operators compete on discipline, not instinct.

The core problem: two calendars, one P&L

Meet Meridian Loom & Trade. 160 people, $74M in revenue, split 42 percent hardware and software (looming equipment and mill operations software sold to 240 mid-size textile mills) and 58 percent marketplace take-rate (on fabric sold through Meridian's B2B marketplace into 1,100 fashion brands, upholsterers, and industrial-textile buyers). The CPO is Vera. The company launched 14 features in 2024 across both sides of the platform.

When Vera classified the 2024 cohort, the distribution told the whole story. Three features were true packaging power (they pushed mills into a higher software tier or moved brand buyers onto a premium marketplace plan). Four were value drivers (they generated real willingness to pay inside the current tier). Five were defensive must-haves (they closed table-stakes gaps competitors had already shipped). Two had no named monetization thesis at all. Those two were killed in review, late, after $2.9M of R&D had already been committed. The kills were the right call. The spend was not.

The deeper problem was not the two dead features. It was the pricing decision cycle. From roadmap vote to locked price and package, Meridian was running a 31-day loop. Engineering committed on day four. Pricing got the specs on day 19. Finance signed on day 29. Sales learned on day 31, which was also the launch week. Two of the largest brand buyers asked why the take-rate moved and nobody had a clean answer, because the meter rationale had been built after the feature was already in code.

Madhavan Ramanujam frames this in Monetizing Innovation. The failure mode is not bad pricing. The failure mode is treating pricing as a last-mile activity. When pricing shows up after the build, the pricing conversation is already lost, because the product was specified for a meter that nobody agreed to. Thomas Nagle and Georg Müller in The Strategy and Tactics of Pricing call this the strategic pricing gap. The gap is the distance between where pricing is decided in the operating model and where it actually creates value, which is upstream of the feature spec.

Marty Cagan in INSPIRED, EMPOWERED, and TRANSFORMED argues that product discovery only works when commercial inputs are in the room from the start. A product team without a live pricing counterpart is a team making commercial bets blind. Melissa Perri in Escaping the Build Trap names the symptom. Output teams ship features. Outcome teams ship monetization. Dan Olsen in The Lean Product Playbook frames product-market fit as a hierarchy, and the pricing conversation is how you know you got that hierarchy right.

Vera's diagnosis was not that her team was bad at product. Her team was good at product. Meridian had no connective tissue between the product calendar and the pricing calendar. The four-part framework is how you build the tissue.

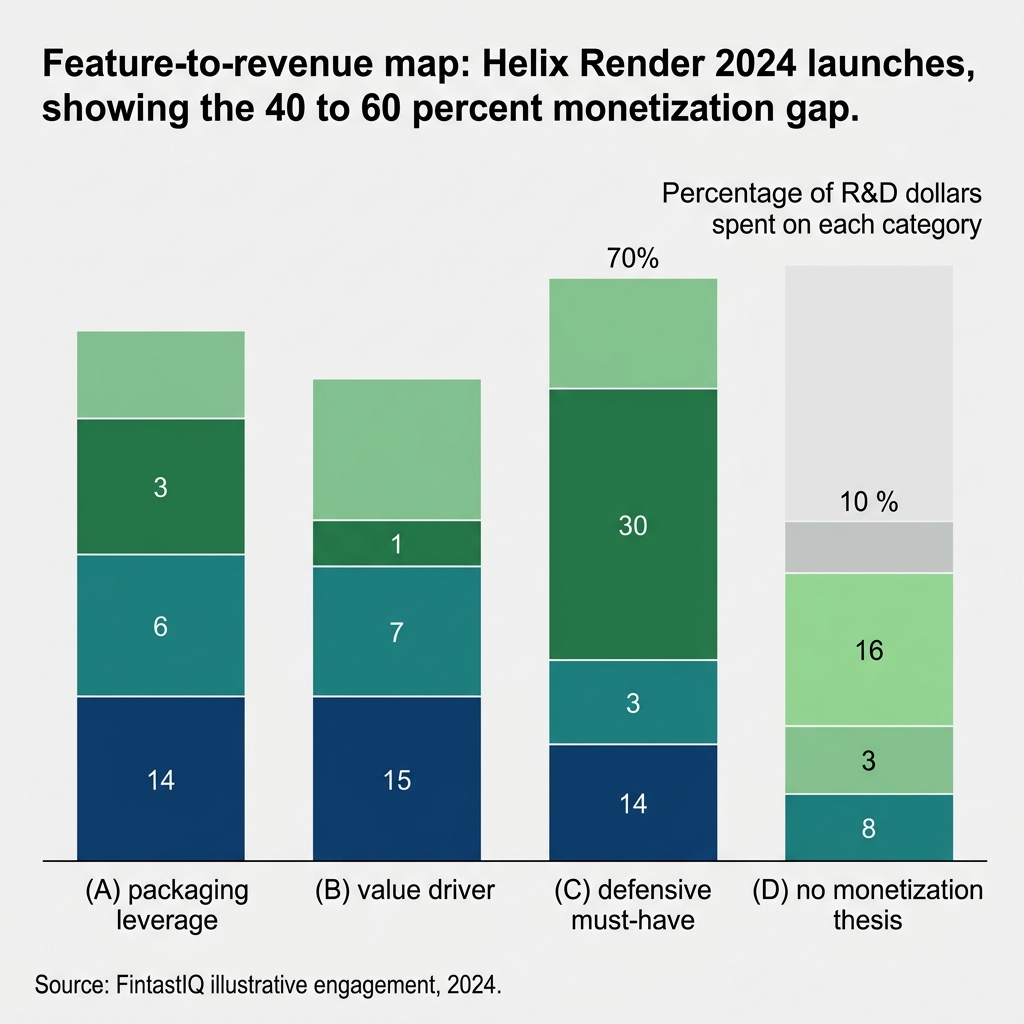

Exhibit: Feature-to-revenue map

Exhibit: Feature-to-revenue map

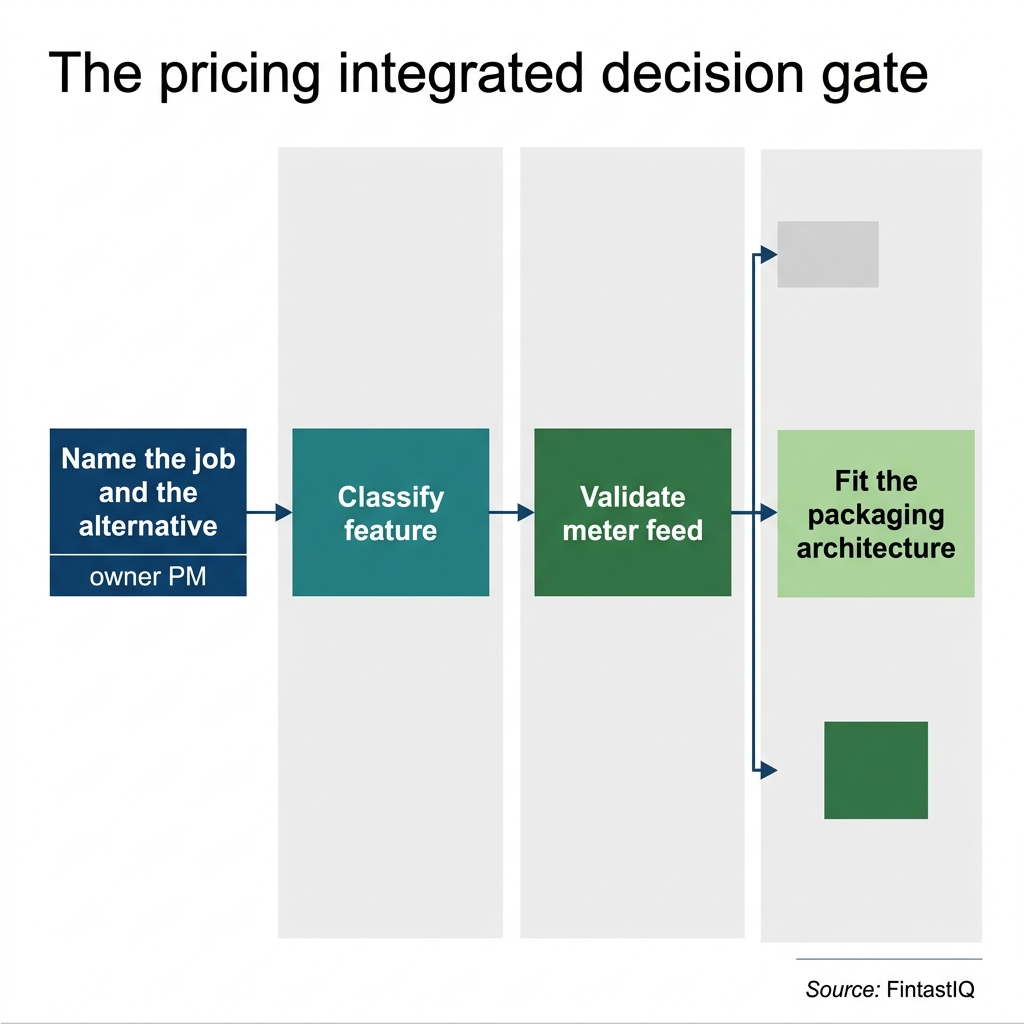

Exhibit: Pricing integrated decision gate

Exhibit: Pricing integrated decision gate

Exhibit: Feature-value classification stacked bar

Exhibit: Feature-value classification stacked bar

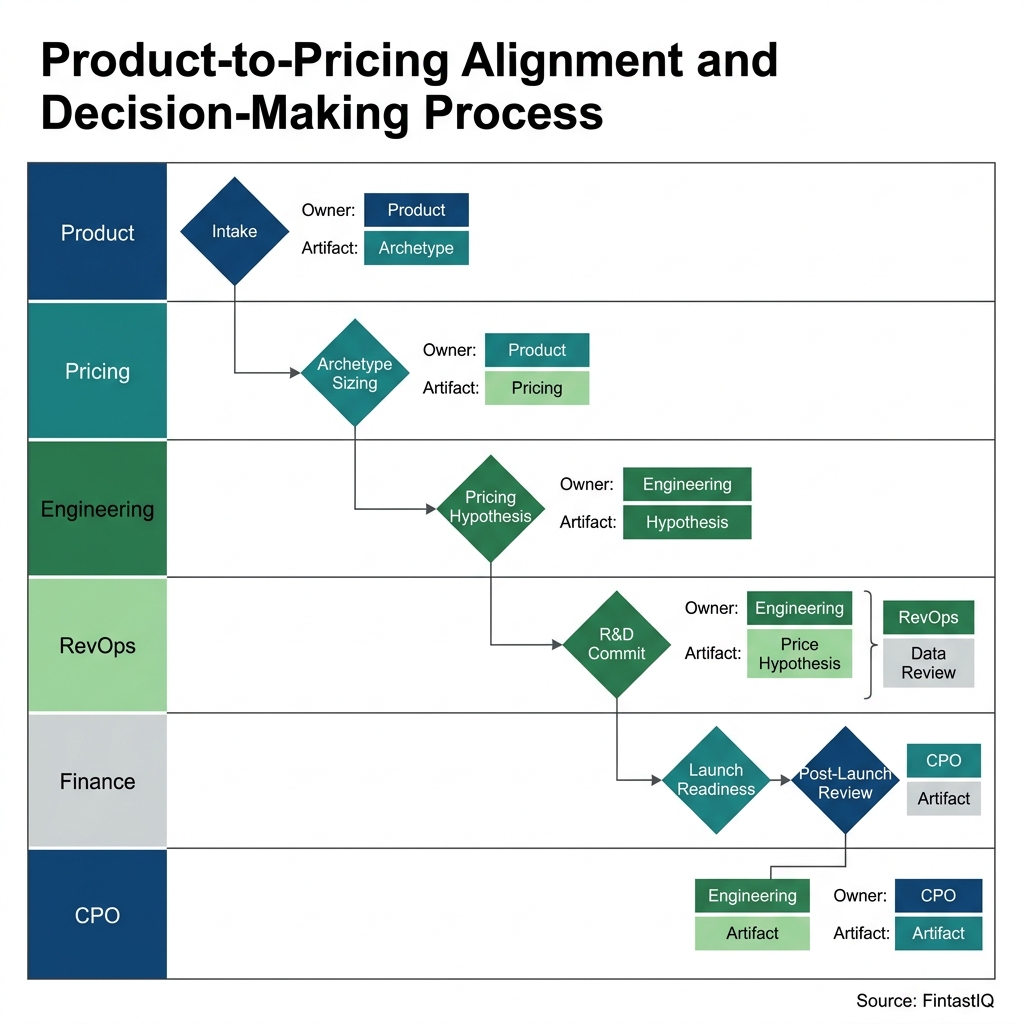

Exhibit: Gate-ceremony flow diagram

Exhibit: Gate-ceremony flow diagram

Part one: classify every feature

Four buckets. Every feature goes into exactly one.

Packaging power. The feature moves buyers between tiers or plans. On the mill side at Meridian, a production-floor analytics upgrade moved 19 mills from the Standard software package to the Professional package inside six months. That is packaging power. The feature has a named tier movement and a measurable mix shift.

Value driver. The feature generates willingness to pay inside the current tier without requiring a tier upgrade. On the marketplace side, a new buyer-side quality guarantee let Meridian defend a 2-point take-rate premium against a lower-cost competitor. That is a value driver. It does not move the package. It defends or expands the meter.

Defensive must-have. The feature closes a table-stakes gap. A competitor shipped it. Procurement asks about it. If you do not have it, you lose deals you should have won. Defensive features do not command a price premium. They protect the ones you already have. Five of Meridian's 2024 features were defensive must-haves, and they were priced correctly (which is to say, not priced separately at all).

No-monetization-thesis. The feature has no named commercial outcome. It might be engineering-driven, executive-championed, or a relic of a deal that closed two years ago. These are the most dangerous items on the roadmap because they consume the same R&D dollars as the three productive buckets without producing anything you can name on the pricing page. Meridian killed two of these in review after spending $2.9M building them. That waste is recoverable once. If the classification discipline is not in place, it recurs every year.

The classification argument is where product and pricing integrate for the first time. The product leader wants to call everything a value driver. The pricing leader wants to call most things defensive. The argument forces both to name their case in language the other will sign. April Dunford in Obviously Awesome makes the same point from the positioning side. The four-bucket rubric is the job test with a price attached.

Part two: run the pricing-integrated decision gate

One ceremony, on the calendar, with a fixed artifact. No engineering commit before the gate clears.

The gate is not a committee. It is a structured review with four signatures. The CPO signs on product thesis. The pricing leader signs on meter and package placement. The CFO or finance partner signs on revenue model and R&D allocation. One frontline seller signs on buyer reaction. Four signatures, one artifact, one decision. The artifact is one page. Feature name. Bucket classification. Named tier or meter movement. Revenue hypothesis for 90, 180, and 360 days. R&D cost. Named retirement trigger if the hypothesis misses. If any field is empty, the feature is not ready for the gate.

Vera ran the first gate at Meridian in Q2. Six gate ceremonies per quarter across product lines (mill software, mill hardware upgrades, marketplace buyer side, marketplace supplier side, platform-wide, and cross-platform data). The pricing decision-gate cycle time dropped from 31 days to 9 days, because the artifact forced every question to the table at once instead of in serial.

Basecamp in Shape Up makes the case for fixed-time, variable-scope ceremonies. The gate is the same idea applied to monetization. You resolve the questions that fit the ceremony. Open questions get named and carried to the next pulse. Forcing resolution produces better decisions than an email thread that drifts three weeks and ends with engineering committing on gut feel.

There are no small features. A small feature shipped into the wrong tier still confuses the buyer, still distorts the meter, still generates a price conversation the seller has to manage. The gate runs for everything above a named threshold (Meridian's threshold is any feature with more than 10 engineering days committed).

Pricing is a signal before it is a number. The gate is where the signal gets set. The number follows.

Part three: feed every decision into the meter-and-package map

The meter-and-package map is the live document that shows every feature, every meter, and every tier. It is updated after every gate ceremony. It is the single source of truth for how the commercial architecture actually looks.

At Meridian, the map has three meters (hardware unit shipments, software seats and active-mill volume, marketplace take-rate percentage) and seven tiers across the two sides of the platform. Every feature sits on the map in exactly one place. Cross-meter features (features that touch both the mill software meter and the marketplace meter) get explicit attention, because they carry the highest revenue impact in the portfolio and are the easiest to underprice.

The 17 percent take-rate lift Meridian captured in 2024 came from one cross-meter feature. A production-floor quality signal that the mill software generated, that then fed into the marketplace to let brand buyers pre-verify fabric quality before ordering. Without the map, the feature would have been priced on one meter (the mill software side) and the marketplace revenue impact would have been captured by the take-rate silently. With the map, the pricing team saw the cross-meter value, repackaged the buyer-side marketplace plan to include the pre-verified quality tier, and lifted the take-rate 17 points on that plan. The 11 percent software ARR expansion on the mill side was a separate line on the same feature, because the mill software repackaging was also visible on the map.

Simon-Kucher research on packaging consistently finds that packaging changes beat pricing changes in customer-friction terms and in revenue terms. Packaging beats pricing. The map is how packaging discipline survives contact with a growing product portfolio. Without the map, you get packaging drift. Tiers accrete features from multiple gate cycles, meters get pointed at features that were never classified as meter-feeders, and the story the seller tells on a call contradicts the story the pricing page tells the self-serve buyer.

McKinsey, Gartner, and Forrester research converge on the same operating-model signal. The format of the map differs (tiers for software, SKU ladders for hardware, take-rate bands for marketplaces), but the discipline is identical. The companies that compound pricing power treat the map as a living artifact, not a deck.

Part four: close the loop with post-launch instrumentation

The gate is a hypothesis. The map is the commitment. The instrumentation is the read.

Every feature that passes the gate ships with telemetry for the named revenue hypothesis. Package-tier mix shift. Meter volume. Take-rate impact. Attach-rate to the tier the feature was intended to move. If the hypothesis lands within 40 percent of the target at day 90, the feature stays as priced and packaged. If it misses by more than 40 percent, the feature re-enters the gate for repackaging, repricing, or retirement. The re-entry is calendar-driven, not discretionary.

Vera built three dashboards for the post-launch loop. One for packaging-power features, tracking tier mix shift. One for value-driver features, tracking meter volume and take-rate. One for cross-meter features. The dashboards are read quarterly at the gate ceremony, not monthly by an analyst who writes a memo nobody reads.

Two features from the 2024 cohort failed the day-90 read. One was repackaged into a different tier and recovered. The other was retired at day 180. The R&D redirected from those two misses plus the two no-thesis kills added up to the $2.9M reinvested into the cross-meter pre-verified-quality feature that produced the 17 percent take-rate lift. The closed loop is the budget line that makes next year's discipline credible to the board.

HBR research on product-market fit arrives at the same frame. Companies that compound pricing power instrument the bet. They do not declare victory at launch and move on. The monetization version of build-measure-learn is more demanding than the engineering version. You are not just learning whether the feature works. You are learning whether the price you promised yourself, the package you placed it in, and the meter you pointed it at actually held up.

Where this framework breaks

Three failure modes. Each one recurs.

Classification theater. The team runs the four-bucket exercise once, declares every feature a value driver or a packaging-power bet, and moves on. The fix is adversarial classification. The pricing leader names the features she would classify as defensive or no-thesis, and the product leader responds in writing. The argument is the point. If every feature comes out of the rubric as a winner, the rubric is not doing its job.

Gate as rubber stamp. The four signatures sign at the end of a week when the artifact shows up on their calendar with a decision already assumed. The fix is the artifact rule. The product lead and pricing lead co-draft the artifact two weeks before the gate. If the artifact is not circulated 72 hours before the ceremony, the ceremony does not run. Empty fields mean the feature is not ready, and "not ready" means engineering does not commit.

Pricing-integrated but not post-launch. The team gets discipline on classification and the gate, ships the features, and then does not instrument the read. The discipline decays within two cycles because nobody can show that last year's gate produced better outcomes than last year's drift. The fix is the day-90 read as a standing item. The same four signatures who signed the gate sit for the day-90 read. If the read is not on the calendar, the loop is not closed.

The 30-60-90 sprint to build product-pricing integration

Days 1 to 30. Classify and draft the gate. Pull every live feature and every in-flight roadmap item. Run the four-bucket classification as a two-day offsite with the product leader, the pricing leader, and a finance partner. Expect the first pass to surface two to five features with no monetization thesis that should not have been committed. Draft the gate artifact template. Pick the first three in-flight features to run through the gate.

Days 31 to 60. Run the first gate and build the map. Schedule the first gate ceremony. Run the three in-flight features through the artifact. Expect at least one to be repackaged or killed in the ceremony. Build the first draft of the meter-and-package map. Every feature, every meter, every tier, one page or one live dashboard. Socialize the map with sales and customer success before the next gate.

Days 61 to 90. Instrument and close the loop. Pick three features from the current launch cohort. Build the day-90 telemetry for each one. Schedule the day-90 read as a standing gate agenda item. Publish the first closed-loop read internally. The read is the artifact that earns the right to run the next cycle.

FAQ

How do we classify features if we have never done it before? Four buckets. Packaging power moves tiers. Value driver generates willingness to pay inside the tier. Defensive must-have closes a table-stakes gap. No-monetization-thesis fails all three. First pass is one day with a product leader and a pricing leader for a 40-feature portfolio. The argument in the room is the integration point.

What is a pricing-integrated decision gate? One ceremony, on the calendar, with a fixed artifact. Four signatures (CPO, pricing lead, finance, one frontline seller). No engineering commit before the gate clears. The artifact names the bucket, the tier or meter movement, the revenue hypothesis, and the retirement trigger if the hypothesis misses.

We sell hardware, software, and take a marketplace fee. Does this work for us? Yes. The meter-and-package map is where hybrid shows up. You run three meters (units, seats or usage, take-rate) and decide which meter each feature feeds. Cross-meter features are the highest-value and the easiest to underprice. Hybrid models need this more than pure-play software.

How do we staff the gate without adding another meeting? Replace, do not add. Collapse your existing roadmap review, pricing committee, and packaging sync into one gate ceremony per product line per quarter. A 160-person company runs roughly six gate ceremonies per quarter and reduces total meeting time.

What if sales wants a feature that fails the monetization thesis? Name the trade in writing. Strategic account concession with a services cost, or a pricing-power investment with a retirement timeline. The gate artifact is the referendum. Escalation goes to CPO and CRO together, not to engineering.

How do we instrument post-launch? Every feature ships with telemetry for its named revenue hypothesis. Tier mix. Meter volume. Take-rate impact. Attach-rate. If the hypothesis misses by more than 40 percent at day 90, the feature re-enters the gate. No loop, no discipline.

Does this apply to consumer durables or hardware-only? Yes. The meter changes, not the discipline. Hardware packages around SKU ladders and attach rates. Consumer durables package around warranty, consumables, and service. The four-part framework holds.

What is the fastest way to start? The 30-60-90 above. Classify the portfolio. Run the first gate. Instrument three features and publish the day-90 read. The muscle is 90 days. The rhythm is quarterly.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

8 QuestionsHow do you classify features by packaging role for the first time?

Run every live feature and every roadmap item through four buckets. Packaging power pushes buyers into a higher tier. Value driver generates willingness to pay inside the current tier. Defensive must-have closes a table-stakes gap. No-monetization-thesis fails all three. The first pass takes a product leader and a pricing leader about one day for a 40-feature portfolio. The argument in the room is the point, because that is where product and pricing actually integrate for the first time.

What is a pricing-integrated decision gate and how is it different from a normal product review?

A normal product review asks whether to build. A pricing-integrated gate asks whether to build, where the feature lives in the package, what meter it touches, and what the named monetization thesis is. It is a single ceremony, scheduled on the calendar, with a fixed artifact. Product, pricing, finance, and one frontline seller all sign. No engineering commit before the gate clears. The gate is the forcing function that prevents the most expensive drift, which is building first and pricing after.

Does product-pricing integration work for hybrid hardware-software-marketplace businesses?

Yes, and the meter-and-package map is where the hybrid shows up. You will have at least three meters live (units shipped, software seats or usage, take-rate percentage) and the package map forces you to decide which meter each feature feeds. Cross-meter features carry the highest revenue impact and are the easiest to underprice, because no single owner sees the full economics. Hybrid commercial models need this discipline more than pure-play software, not less.

How do you staff a pricing-integrated decision gate without adding another standing meeting?

Replace, do not add. Most teams already run a roadmap review, a pricing committee, and a packaging sync on separate calendars. Collapse them. The gate is one 60 to 90 minute ceremony per quarter per product line, with a short weekly pulse between gates for in-flight features. A 160-person company typically runs six gate ceremonies per quarter across product lines and reduces total standing meeting time, not adds to it.

What do you do when sales wants a feature that fails the monetization thesis?

Name the trade in writing. Either it is a strategic account concession with a services-contract cost attached, or it is a pricing-power investment the company is choosing to make with a timeline for retirement if it never earns a thesis. Do not let sales informally set the roadmap by winning the last deal. The gate artifact is the referendum. Sales signs or escalates, and the escalation goes to the CPO and CRO together, not to engineering.

How do you instrument post-launch revenue so the product-pricing loop closes?

Every feature that passes the gate ships with a named revenue hypothesis and the telemetry to test it within 90 days. Package-tier mix shift. Meter volume. Take-rate impact if the feature touches marketplace economics. Attach-rate to the named tier. If the hypothesis misses by more than 40 percent at day 90, the feature re-enters the gate for repackaging or retirement. Without the loop, the gate is theater.

Does product-pricing integration apply to consumer durables or hardware-only businesses?

Yes. The meter changes, not the discipline. Hardware companies package around SKU ladders, accessory attach, and service tiers. Consumer durables package around warranty, consumables, and post-purchase service. The four-part framework holds. A feature decision on a dishwasher or a looming machine is still a pricing decision because it moves SKU ladder economics and attach rates, even without a subscription in sight.

What is the fastest 30-60-90 way to start product-pricing integration?

A 30-60-90 sprint. Days 1 to 30 classify every live feature and in-flight item into the four buckets and draft the gate artifact. Days 31 to 60 run the first gate ceremony and kill or repackage at least two in-flight items. Days 61 to 90 instrument three launched features with post-launch telemetry and publish the first closed-loop read. The muscle is 90 days. The rhythm is quarterly.

Every feature decision is a pricing decision, whether your operating model admits it or not. Most product and pricing teams run parallel calendars, trade artifacts at the end, and ship features that never earn what the roadmap promised. The discipline is a four-part integration: classify every feature by packaging role, gate it inside a pricing-integrated ceremony before engineering commits, feed the decision into the meter-and-package map, and close the loop with post-launch revenue instrumentation. Packaging beats pricing. Pricing is a signal before it is a number.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- Madhavan Ramaswamy & Georg Tacke. Monetizing Innovation. Wiley, 2016

- Marty Cagan. Inspired. Wiley, 2018

- Thomas Nagle & Georg Müller. The Strategy and Tactics of Pricing. Routledge, 2016

- Wes Bush. Product-Led Growth. Product-Led Institute, 2019

- Rafi Mohammed. The Good-Better-Best Approach to Pricing. Harvard Business Review, 2018