$95M Off the Bid: 5 Diligence Layers on a Coldflux HVAC Deal

Conventional top-down commercial due diligence tends to flatten hybrid businesses into a single narrative, which hides the channel, pricing, and pipeline risks that determine post-close outcomes. This paper lays out a five-layer signal-seek framework used by disciplined deal teams to pressure-test market, customer, product-pricing, pipeline, and team claims before LOI. It walks through a recent Meadowline Capital engagement on Coldflux HVAC to show how the layers generate a defensible bid, a negotiation posture, and a post-close commercial plan.

Commercial Due Diligence Signal-Seek Layers: A Framework for Hybrid-Revenue Targets

Most commercial due diligence reports read the same way. A market section that everyone skims. A customer section built on ten references. A financial appendix that nobody ties back to the commercial story. A recommendation that says proceed with the following risks, where the risks are the same three risks every deal has. The report is thick, the team is confident, and the acquirer finds out after close that the real risk was in a dimension the report barely touched.

This happens most often in hybrid-revenue targets: businesses that mix hardware, services, marketplace, and subscription economics. The blended P&L hides where the economics break. The narrative the seller brings flatters the stream that trades at the highest multiple. The diligence team works hard on the market story because that is what the IC likes to see, and the channel, pricing, and pipeline signals get skimmed.

The framework in this paper is the counter. We call it signal-seek layers because each layer forces the diligence team to seek a specific signal before synthesizing anything. Five layers, each with its own question, its own method, and its own deliverable. The test of a layered run is not whether the report reads well; it is whether the bid, the negotiation posture, and the post-close plan all hold together when the seller pushes back.

TL;DR

Hybrid-revenue targets punish top-down commercial due diligence because the blended view hides the stream that carries the real risk. The signal-seek framework uses five layers: market, customer, product-pricing, pipeline, and team: each with a narrow question and a defined deliverable, so the diligence output is a bid rationale and a post-close plan rather than a report. The Meadowline Capital engagement on Coldflux HVAC shows how the layers surface channel risk, pricing leakage, and undisclosed product changes, and how those findings translate into a 20 percent under-asking bid with two post-close commercial imperatives.

Exhibit: Signal-seek layer matrix

Exhibit: Signal-seek layer matrix

Exhibit: Cohort-vintage heatmap (Layer 4 deep-dive)

Exhibit: Cohort-vintage heatmap (Layer 4 deep-dive)

The Core Problem: Why Top-Down CDD Misses Commercial Risk

Top-down commercial due diligence was built for a cleaner era. A single revenue model, a definable market, a sales team that looked like every other sales team in the category. When a target fit that shape, scoring it against the category was a reasonable approximation of commercial health. The method persisted long past the businesses that justified it.

Hybrid-revenue targets break the method in four places. First, the market is actually several markets with different growth rates, different competitive dynamics, and different buyer behaviors, and averaging them produces a number that describes nothing. Second, the customer is actually several stakeholder types, often with conflicting interests: the end customer who consumes the product, the channel partner who installs it, the operator who manages the service. Third, pricing is a composite of several billing mechanisms, some of which are tracking value and some of which are tracking accounting history. Fourth, the pipeline is actually several pipelines with different velocities, and the blended conversion rate means nothing operationally.

Pricing is a signal before it is a number. When we see a hybrid target with seven billing dimensions, our first question is not what the price is; it is whether customers can name the dimensions. If they cannot, the revenue line is structurally fragile regardless of what the growth curve shows, because the business is extracting value from confusion rather than from captured value. Confusion is the enemy of willingness to pay, and it is the enemy of renewal, and it is the enemy of the expansion motion that the seller is almost certainly pitching.

This paper uses a recent engagement to make the framework concrete. Meadowline Capital, a mid-market PE firm with $1.2B AUM, engaged us as the lead commercial diligence partner on their evaluation of Coldflux HVAC. Coldflux is a hybrid HVAC-controls business: hardware product, B2B2B installer marketplace, and a managed-service subscription to building owners, with roughly 32 percent of revenue in hardware, 28 percent in marketplace take-rate, and 40 percent in subscription. Coldflux has 200 people, $140M revenue, 3,800 active installer partners, and 18,000 end-customer accounts. The company was founded in 2014, had been owned by a prior fund for six years, and was being brought to market by the seller at a $475M asking price. Meadowline's deal team was led by Operating Partner Sian, who had run two prior portfolio companies in the building-systems category and insisted on a layered approach from the outset.

What follows is how the five layers were built, what each found, and how the findings translated into a bid of $380M, a forty-day negotiation, and a close at $395M with two named post-close commercial imperatives.

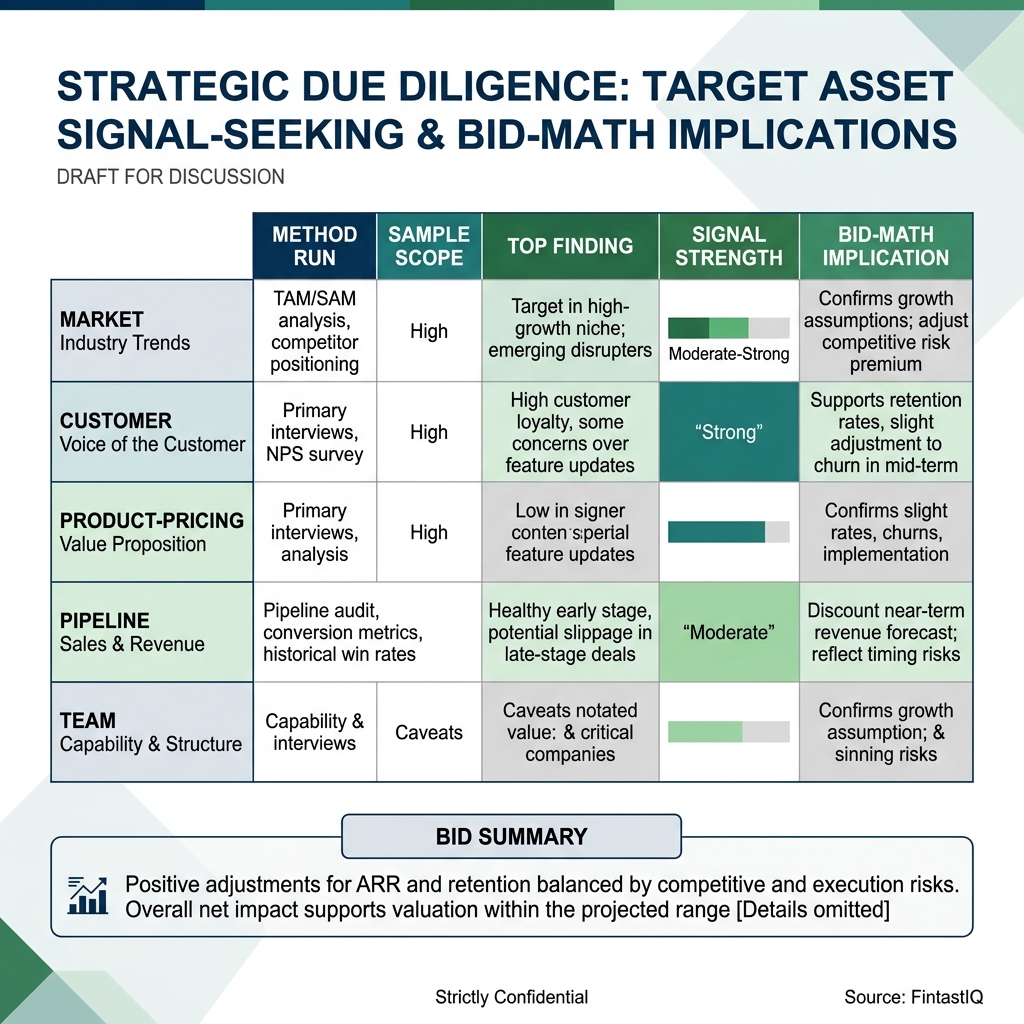

The Five Signal-Seek Layers

Why layers beat checklists for hybrid archetypes

A checklist tells the team what to look at. A layer tells the team what question to answer before moving on. The difference is not semantic. Checklists generate coverage; layers generate decisions. In a hybrid target, coverage without decisions produces a report that describes the company without committing to a view, and the IC cannot price what the team will not commit to.

The second reason layers work is stacking. Each layer's finding becomes context for the next layer's interrogation. The market layer finds that the retrofit sub-segment is growing three times the blended market rate, which reframes the customer layer to ask whether the target is actually winning in retrofit specifically. The customer layer finds that installer NPS is weak, which reframes the pipeline layer to ask whether recent pipeline growth is channel-dependent. Layers build on each other; checklists sit side by side. The best operators compete on discipline, not instinct, and layered diligence is the discipline version of the same activity.

Layer 1: Market: re-underwriting the TAM, not accepting it

The seller's CIM presented the HVAC-controls market at 6 percent growth, cited two industry reports, and moved on. Meadowline's team did not move on. They decomposed the market into four sub-segments by building type and by new-build versus retrofit, pulled five years of building-permit data, triangulated against HVAC distributor reports, and rebuilt the growth rate by sub-segment.

The finding reframed the deal. The overall HVAC-controls market was indeed growing at 6 percent. The retrofit sub-segment Coldflux actually played in: commercial buildings over 50,000 square feet retrofitting controls onto existing HVAC infrastructure: was growing at 14 percent, driven by energy-code tightening in seven states and by utility rebate structures that had shifted in 2023. The seller had under-told the market story because the seller's own segmentation was not that granular.

This is a rare but important finding: the market was actually better than the seller claimed. Meadowline did not adjust the bid up for this; the team adjusted their conviction up. A 14 percent segment tolerates more operational investment than a 6 percent segment, which changed the calculus on the post-close commercial imperatives we describe later.

Layer 2: Customer: separating the end user from the channel

The most consequential decision in customer diligence is who counts as the customer. For Coldflux, the easy answer was the building owner who signed the subscription contract. The right answer was both the building owner and the installer who chose which controls platform to recommend. Those two stakeholder groups had different incentives, different satisfaction drivers, and different substitution options, and collapsing them would have produced a misleading signal.

The team ran 23 win-loss-churn interviews: 14 with end customers, 9 with installer partners, spanning wins, losses, and churns across the last 18 months. The end-customer NPS was 52, which is strong. The installer NPS was 19, which is a distress signal.

The installer conversations surfaced three specific drivers: a commission structure change in late 2023 that installers experienced as a pay cut, a technical-support SLA that had slipped from 4-hour response to next-day response in practice, and a growing sense that Coldflux was competing with its own installer channel on larger accounts through a direct sales team stood up in 2024. Any one of these would have been a repairable irritant; together they had created a channel risk that the seller had not disclosed and that the CIM did not mention.

The commercial implication was direct. Roughly 28 percent of Coldflux's revenue flows through installer-originated accounts. If installer NPS continues to slide, marketplace take-rate revenue is at material risk on a 12-to-18-month horizon. The customer layer, in other words, reframed the commercial risk of the deal: the real risk was channel, not customer.

Layer 3: Product-Pricing: deconstructing the subscription meter by meter

The subscription revenue stream is the multiple-bearing stream in a hybrid target, and the seller's CIM had presented it with the confidence that comes from strong headline metrics. The team's question was not whether the metrics were accurate; the question was whether the pricing mechanism was durable. Pricing maturity is measured by what you stop doing, and weak pricing mechanisms are usually thick with dimensions that nobody remembers adding.

The team took the subscription apart meter by meter. Seven billing dimensions: per-building base fee, per-zone uplift, per-energy-saved dollar share, per-API-call overage, per-user seat fee, per-mobile-access fee, per-annual-reporting fee. The team asked customers to describe what they were paying for. End customers could name three of the seven with confidence: the base fee, the energy-saved share, and the seat fee. They could not describe the other four, did not know they were being charged for them, and in two cases did not know the features existed.

Three billing dimensions out of seven were tracking nothing end customers valued. They contributed roughly 9 percent of subscription revenue, which is both too small to matter for the bid mechanics and too large to ignore for the post-close plan. If a pricing audit surfaced these dimensions to customers, some would churn the dimensions; if competitors surfaced them, some would churn the subscription. The pricing layer produced a specific post-close imperative: retire or reshape three billing dimensions in the first sixty days, with a contract-transition motion that converts the revenue to a dimension customers can describe.

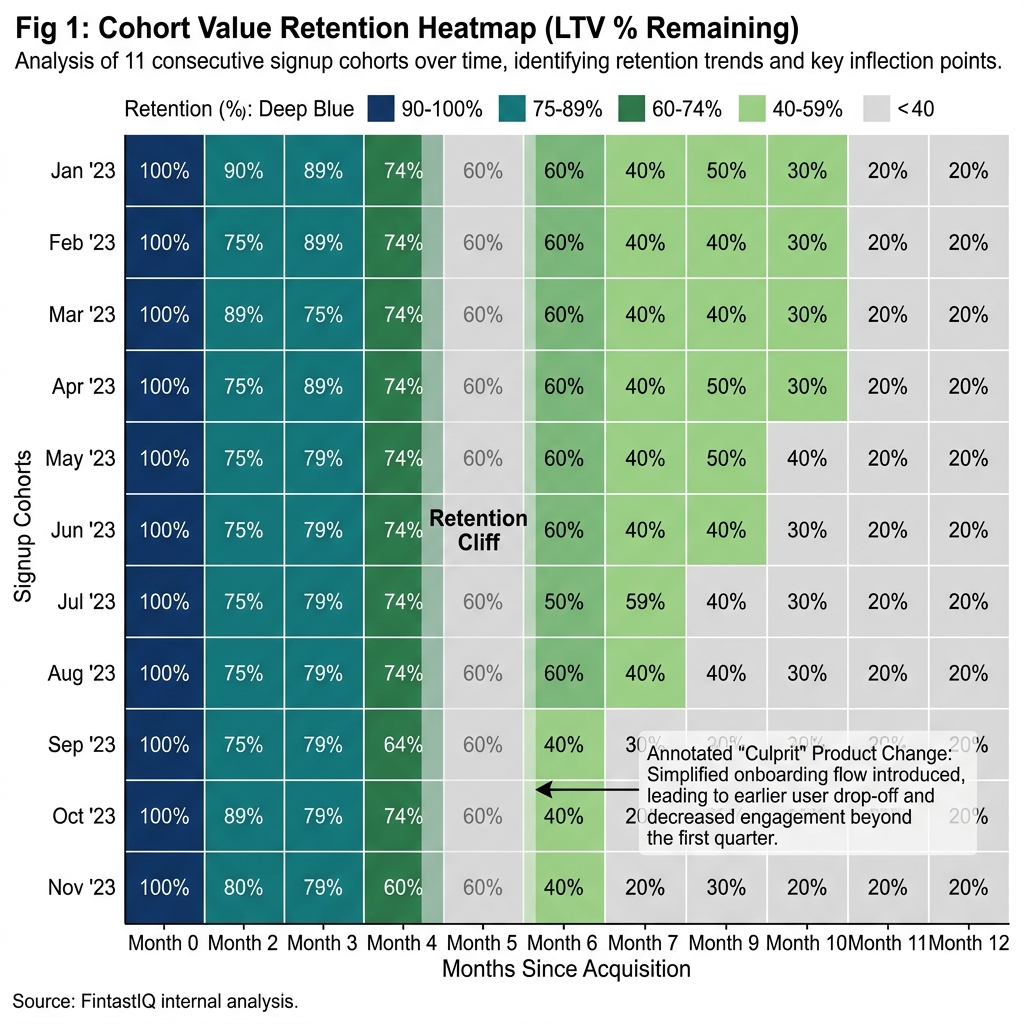

Layer 4: Pipeline: vintage analysis of 11 cohorts

A blended retention number is a summary statistic of a question the team has not yet asked. The question is whether each cohort behaves like the last, and if not, which cohort broke the pattern and why. The method is vintage analysis: take each quarterly customer-acquisition cohort, plot its retention curve, and look for the one that bends.

The team ran vintage analysis across 11 cohorts spanning Q1 2022 through Q3 2024. The first nine cohorts had retention curves that were statistically indistinguishable: ninety-day retention around 91 percent, twelve-month retention around 78 percent, eighteen-month retention around 71 percent. The tenth cohort, Q2 2024, looked like the prior nine. The eleventh cohort, Q3 2024, bent. Ninety-day retention dropped to 82 percent, twelve-month retention was tracking toward 66 percent, and the bend was too sharp to be explained by cohort composition or seasonality.

The team went back to Coldflux's product changelog and found a March 2024 release that modified the default commissioning workflow for new accounts. The change had not appeared in the CIM; it had not appeared in the management presentations; it had not appeared in the data room's product section because the product section did not include a changelog. The seller's position, when asked, was that the change had been reverted in October 2024 and that retention was recovering. The team could not confirm the recovery because not enough post-reversion vintage existed.

This finding did not kill the deal, but it changed the posture. The bid would now reflect the uncertainty in the Q3 2024 cohort's normalization. If retention recovered, the acquirer would capture upside. If retention did not recover, the acquirer had already priced the risk. Either way, the seller could not pretend the issue did not exist.

Layer 5: Team: reference calls on the commercial leadership

The team layer is the one most diligence programs run last and shortest, because it feels softer than the others. The experienced teams run it first and longest. A weak commercial leader in a strong business is a solvable problem; a strong commercial leader in a weak business is a rescue mission.

The team ran 9 reference calls on the Coldflux commercial leadership: the CRO, two VPs of sales, the head of marketing, the head of customer success, the head of installer partnerships, and three prior reports. The surfacing finding concerned the CRO, who was 11 months into the role at the time of diligence. The CRO had a credible track record and strong references, but three signals converged: the commercial team was still being built, the hiring plan on paper was four heads behind what the CRO had been asked to deliver, and two of the VPs had joined within the last six months and had not yet had a full sales cycle under their belts.

The team's view was not that the CRO was wrong for the company. The view was that the commercial organization was earlier in its maturity than the seller's narrative implied, and the hiring plan was a leading indicator that the CRO was aware of the gap but had not yet been funded to close it. Post-close, the acquirer would need to support either faster hiring or revised targets; the two would not be independent.

Synthesis: Pricing the Risk, Not Just the Asset

The five layers do not independently produce a bid. Synthesis produces the bid. The synthesis question is not what the asset is worth; it is what the risk is worth to carry, and at what price the acquirer is willing to carry it. The seller's asking price of $475M implied that the market was good, the customer was good, the pricing was durable, the pipeline was stable, and the team was built. The layer findings said: market is better than advertised, customer is good but channel is at risk, pricing has structural leakage, pipeline has an undisclosed cohort break, team is earlier in maturity than advertised.

The team priced each finding. Market upside added conviction, not value. Channel risk subtracted approximately $40M through a combination of marketplace take-rate haircut and installer-remediation cost. Pricing leakage subtracted approximately $12M on a discounted-cash-flow basis reflecting the contract-transition period. Pipeline uncertainty subtracted approximately $28M reflecting a probability-weighted retention trough on the Q3 2024 cohort. Team maturity subtracted approximately $15M reflecting six months of incremental hiring cost and delayed quota ramp. The blended bid landed at $380M, 20 percent below the seller's ask.

The bid letter accompanied a specific negotiation posture: Meadowline was prepared to move modestly on price if the seller could address three items in diligence Q and A, and modestly further if the SPA reflected appropriate representations on the March 2024 product change. After a 40-day negotiation, the deal closed at $395M with expanded reps around the pipeline cohort and explicit post-close cooperation commitments from the seller on the installer-channel situation.

Post-Close Handoff: Artifacts That Carry the Findings Forward

A diligence finding that does not reach the hundred-day plan is a finding that did not happen. The handoff from diligence to operating is where most PE commercial-diligence programs lose the thread; the report gets archived, the team that ran the layers disperses, and the operating partner starts from scratch. Meadowline's model avoided this by building two artifacts during diligence that were explicitly post-close instruments.

The first artifact was the commercial imperatives list: a running list of named actions with owners, metrics, and timelines, updated during diligence and handed to the CEO and CRO on day one. The Coldflux list had two tier-one imperatives: installer NPS recovery from 19 to 40 by day 90, with the head of installer partnerships owning, and billing-dimension simplification from seven to four by day 60, with the CFO and head of product co-owning. Both imperatives had weekly scorecards drafted during diligence and handed over on signing.

The second artifact was the diligence signal map: a one-page diagram showing how each layer's finding connected to each commercial imperative, so the CEO could trace any operating decision back to a diligence signal. This sounds bureaucratic; in practice it was the reason the 100-day plan did not drift. When board discussion raised a question about whether to accelerate direct sales, the signal map reminded everyone that direct-sales acceleration was one of the installer-NPS drivers, and the answer was to pace the direct motion rather than drop the imperative.

Three Failure Modes

Over-indexing on one layer

The failure is familiar. A diligence team falls in love with the market layer because it is the most presentable, or the customer layer because the quotes are vivid, and the other layers get abbreviated. The countermeasure is a layer-weight discipline at the start: each layer gets a named lead, a named budget, and a named deliverable, and the synthesis meeting cannot start until every layer has delivered. Meadowline enforced this with a simple rule: any layer missing its deliverable at synthesis pushed synthesis by a week. The rule was invoked twice during the Coldflux run and both times improved the final view.

The seller's narrative sneaks back in

Diligence teams are human, and the seller's narrative is often well-told. In the back half of a deal, as the IC date approaches and the team has built a rapport with management, negative findings soften. The countermeasure is to name the findings as findings, not opinions, and to restate them verbatim in the synthesis deck in the language the layer produced them. If the customer layer produced the phrase the real commercial risk is channel, not customer, the synthesis deck uses that exact phrase. The discipline feels rigid; the outcomes are more defensible.

Post-close forgets the findings

The third failure is the handoff failure described above. The countermeasure is the artifact discipline: no diligence engagement concludes without a commercial imperatives list and a signal map, and those artifacts are named as post-close deliverables in the diligence scope. Reporting this as a line item in the engagement's scope of work changes the team's behavior: findings get written with the imperatives list in mind, and imperatives get written with the post-close owner in mind.

30-60-90 Sprint: IC-Timed from Pre-LOI to Post-Close 100 Days

Days -45 to -30 (pre-LOI): Scope the five layers with named leads. Build the market decomposition and the team reference list. Begin customer reference outreach; hybrid targets need lead time to reach installers and secondary stakeholders.

Days -30 to -15: Run layers one and two to saturation. Seat the product-pricing and pipeline analysis on data-room access. Draft the first version of the commercial imperatives list based on emerging signals.

Days -15 to LOI: Synthesize across all five layers. Write the bid rationale, the negotiation posture, and the draft hundred-day plan. Issue the LOI.

LOI to close (typically 30-60 days): Refine imperatives based on confirmatory diligence. Finalize the signal map. Align the acquirer's operating partner, the incoming CEO, and the CRO on imperatives, metrics, and owners.

Close to day 30: Handoff meeting with the full commercial team. Install weekly scorecards for each imperative. Begin the installer-NPS and billing-dimension work streams in parallel.

Days 30-60: Billing-dimension simplification reaches its milestones; first wave of customer contract transitions underway. Installer-partnership changes announced; channel stabilization begins.

Days 60-90: Installer NPS re-measured. Billing dimensions reduced. Pipeline cohort tracking installed. First board report to the investment committee tied to signal-map imperatives rather than general operating metrics.

What We Do not Share Publicly

We do not share the specific reference-call protocols we use for installer and channel-partner conversations; the value of those protocols lies in the questions we do not ask as much as the ones we do. We do not share our pricing-dimension deconstruction template because the version we use reflects client-specific calibrations built over many engagements. We do not share our vintage-analysis code because the interesting judgment is in how we handle cohort-composition adjustments, and that judgment is not reducible to code. Clients who engage us get the protocols, the template, and the analysis; readers of this paper get the framework and the findings.

FAQ

What is a signal-seek layer in commercial due diligence? A signal-seek layer is a defined analytical cut of the target that forces the diligence team to answer a specific commercial question before synthesis. Each layer forces a narrower interrogation than the generic question of whether this is a good company. Layers prevent a strong narrative in one dimension from obscuring a weak signal in another. In hybrid-revenue targets, layers matter more because economics differ by stream and a blended view hides where the real risk lives.

Why do hybrid-revenue businesses need a different diligence approach? Hybrid-revenue businesses mix hardware, services, marketplace, and subscription economics inside a single P&L. A top-down approach tends to score the company on the dominant narrative the seller wants told. A layered approach forces evaluation of each stream on its own terms and examines the seams between them, which is usually where channel risk, pricing risk, and retention risk live.

How many customer references should a commercial diligence program run? Twenty to thirty is a reasonable floor for a hybrid target. The goal is not statistical significance but saturation: the point at which new interviews stop generating new themes. For the Coldflux engagement, Meadowline ran 23 win-loss-churn interviews and thematic saturation appeared around interview 17.

How do you price channel risk into a bid? Through the multiple applied to channel-dependent revenue and the size of the post-close channel-repair investment. The Coldflux bid reflected roughly 20 percent of the gap as channel remediation and the rest as pipeline and pricing uncertainty.

What does pricing diligence look like pre-LOI? A meter-by-meter deconstruction of how the target captures value. The team maps every billing dimension and tests whether customers can articulate what they are paying for. When customers cannot name the units they are buying, pricing is weak regardless of what the revenue curve shows.

How should diligence findings translate to a post-close plan? Through named commercial imperatives with owners, milestones, and metrics. A finding that installer NPS is 19 becomes a 90-day imperative to reach 40. The handoff artifact is a running list that the operating partner, CEO, and CRO pull from during the first board cycle.

What are the most common failure modes in commercial diligence? Over-indexing on one layer, allowing the seller's narrative to sneak back in during synthesis, and losing the findings at handoff. Each has a specific countermeasure described in the framework.

How long should a five-layer diligence run? For a mid-market hybrid target, four to six weeks from engagement to bid. Market and team layers run in parallel in the first two weeks; customer references take two to three weeks; product-pricing and pipeline layers run in weeks three and four; synthesis and bid prep occur in weeks five and six.

Run the free assessment or book a consultation to apply this framework to your specific situation.

Questions, answered

3 QuestionsWhat is a signal-seek layer in commercial due diligence?

A signal-seek layer is a defined analytical cut of the target that forces the diligence team to answer a specific commercial question before synthesis. Each layer forces a narrower interrogation: is the market growing where this target plays, are customers recommending the product, is pricing capturing value, are cohorts behaving, is the team credible. Layers prevent the common failure where a strong narrative in one dimension obscures a weak signal in another.

Why do hybrid-revenue PE targets need a different commercial diligence approach?

Hybrid-revenue businesses mix hardware, services, marketplace, and subscription economics inside a single P&L. A top-down approach tends to score the company on the dominant narrative the seller wants told, almost always the subscription stream because it trades at the highest multiple. A layered approach forces evaluation of each stream on its own terms and then looks at the seams between them, which is usually where channel risk, pricing risk, and retention risk all live.

What does pricing-specific commercial due diligence look like pre-LOI?

Pre-LOI pricing diligence is a meter-by-meter deconstruction of how the target captures value. The team maps every billing dimension, every list-to-net leakage, every contractual concession, and tests whether customers can articulate what they are paying for. When customers cannot name the units they are buying, pricing is weak regardless of what the revenue curve shows. The deliverable is a pricing maturity score and a list of dimensions the acquirer should keep, reshape, or retire in the first one hundred days.

Conventional top-down commercial due diligence tends to flatten hybrid businesses into a single narrative, which hides the channel, pricing, and pipeline risks that determine post-close outcomes. This paper lays out a five-layer signal-seek framework used by disciplined deal teams to pressure-test market, customer, product-pricing, pipeline, and team claims before LOI. It walks through a recent Meadowline Capital engagement on Coldflux HVAC to show how the layers generate a defensible bid, a negotiation posture, and a post-close commercial plan.

How relevant and useful is this article for you?

About the Author(s)

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

Emily Ellis is the Founder of FintastIQ. Emily has 20 years of experience leading pricing, value creation, and commercial transformation initiatives for PE portfolio companies and high-growth businesses. She has previous experience as a leader at McKinsey and BCG and is the Founder of FintastIQ and the Growth Operating System.

References

- William Thorndike. The Outsiders. Harvard Business Review Press, 2012

- Bruce Greenwald & Judd Kahn. Competition Demystified. Portfolio, 2005

- Eileen Appelbaum & Rosemary Batt. Private Equity at Work. Russell Sage Foundation, 2014

- Bain & Company. Global Private Equity Report. Bain & Company, 2024

- McKinsey & Company. The Power of Pricing. McKinsey Quarterly, 2003